tl;dr: It was the best of times, it was the worst of times.

The 2016 tech market is a confusing place.

Public tech stocks took a beating early in the quarter, leading to fear of a dramatic valuation correction. Sentiment was sufficiently negative that it was impossible to avoid the topic over cocktails, and Mattermark took the step of publishing notes on how startups could avoid dying.

{kind=link}

Then things, oddly enough, got better. The NASDAQ recovered, bouncing back towards the historically-critical 5,000 mark. DoorDash raised $127 million in a single shot. It became clear that while the venture capital market—and therefore the startup capital cycle—had changed at least some, things remained heated.

Results from the now-closed quarter bear that out. Investors raised more money in the first quarter of 2016 than in the first quarter of 2015. Startups received nearly precisely the same amount of capital from investors in the first quarter of this year as they did the last, a sum above historical averages. And 2015’s technology IPO crop staged a comeback putting the group nearly back to their sale prices.

Layoffs appeared to slow as the quarter ended, and the IPO market may manage to unfuck itself in short order. All told, things are looking up. Perhaps.

On the other side of the coin is the fact that there have been zero United States-based technology IPOs this year, M&A activity looks weak, and we’ve seen a dramatic retrenchment in valuation multiples, devaluing public companies before their private analogs have had to reprice through the raising of new capital. We could be living through a case of chaos deferred.

If all that sounds a bit confusing, I understand. Happily, Mattermark has reported on various parts of the above information all year so we have context to share. Let’s take a macro look today to understand what is good, what is bad, and what could become ugly.

The Good

Ice cream first, I think.

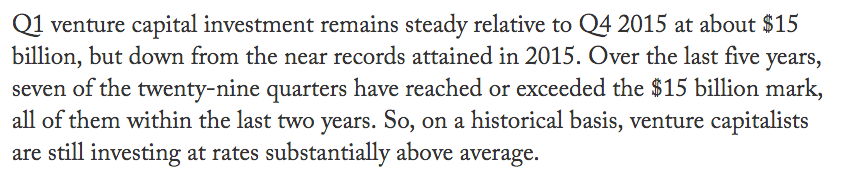

Total global venture capital expended in the first quarter totaled $30 billion. That’s down a mote from the 2015’s first quarter tally of $31.8 billion. But don’t worry: venture capital investing in the United States, to pick an example, remains elevated over historical norms. As Tomasz Tunguz points out:

{kind=link}

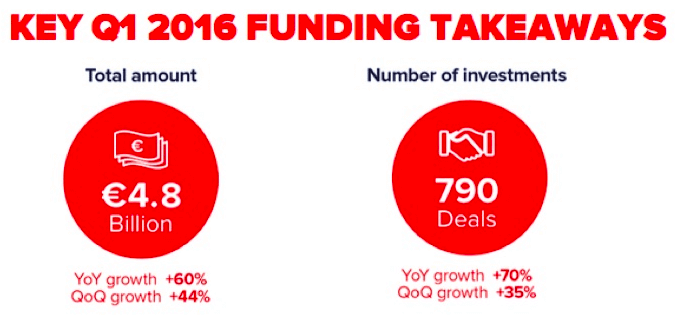

Across the pond, the European venture capital market recorded impressive gains in the first quarter. According to Tech.eu, things were solid indeed:

Will that last? As it turns out, venture capitalists aren’t merely disbursing huge sums, but they are collecting more ammunition than they were a year ago. Venture crews raised $16.7 billion in the first quarter of 2016, up from $13.1 billion in 2015’s first three months.

In the United States alone, according to the National Venture Capital Association, VCs raised $12 billion in the first quarter—more than the prior two quarters combined. We’re not done seeing a faster-than-average investment cadence in dollar terms.

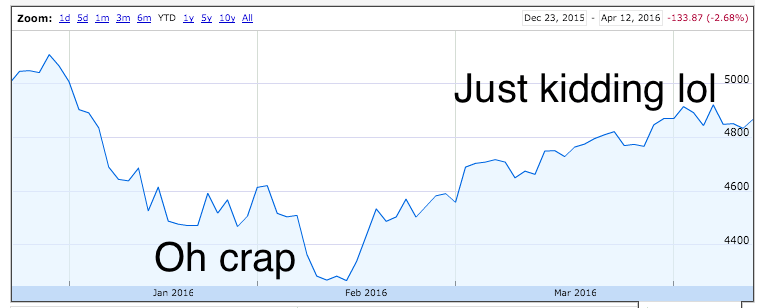

Turning from the private to the public markets, the NASDAQ has recovered from the low 4,000s to the high 4,000s, erasing most of its year-to-date losses.

Those gains also apply to recent IPOs. After a rough start, the 2015 crop of technology IPOs that Mattermark tracks are nearly back to their initial price. They are down from their first day closes, naturally, but they have made progress towards equilibrium.

What’s the result of that? Well, the IPO pipeline is finally starting to fill. SecureWorks could be followed by Domo. That’s not a huge amount of traffic, but it’s certainly more than zero. Add in fewer publicly-noted layoffs and it’s almost like that entire dip didn’t happen. Aside from the fact that it did, of course.

To summarize all of that, I’ve prepared a very technical chart explaining the NASDAQ’s performance in 2015. You will understand it at a glance:

The Bad

If there are a host of positive signals to enjoy, there is a different set to the contrary.

To pick one example, seed round dollar volume is down, and dollar volume of $100 million checks that don’t top $1 billion are down as well. That squeezes the startup market on both ends.

You don’t need an open IPO window for the market to provide liquidity to investors and startups alike. However, you do need M&A activity. If you have active acquisition activity and public offerings, all the better. However, we certainly do not have the latter at the moment.

So, how about M&A? Things don’t look that great. According to one report, technology M&A activity eased around 30 percent in the first quarter, compared to the year-ago period.

Adding to that list is fear that some of the positive things that the market is seeing could end up being net-negatives. Investing cadence back up? Could be bad. Lots of new venture capital raised from LPs? That could be bad as well. And that’s according to some venture capitalists themselves.

Here’s Semil Shah discussing the rapid improvement in market pace in March:

Startup financing market update: 80% of people have entirely forgotten what happened in public markets in January & February.

— Semil (@semil) March 11, 2016

And Bill Gurley reacting to an investing group raising a new fund north of $1 billion:

Completely disagree. Excess capital is really bad for founders. Leads to excessive competition and poor returns. https://t.co/j3zy71nqDh

— Bill Gurley (@bgurley) April 12, 2016

Let’s translate Gurley. If you have a set of companies looking to raise, and on the other side of the equation add more available capital what will happen to pricing? Same supply, more demand. That can lead to higher valuations than otherwise might make sense, and lower returns for venture kids.

How is that sort of competition bad for entrepreneurs? If you raise at too high a valuation and fail to grow into it, you could have given yourself a bit too much rope.

The Ugly

Parsing through media reports, sentiment, and activity in the first quarter today, it struck me how connected the public and private markets are in terms of sentiment. Private companies will never reprice as quickly as their public counterparts, due to how their shares trade. But the link between dramatic declines in the NASDAQ and sentiment among the private sector appeared far more in sync.

For our purposes, that means if the NASDAQ faints again, we could be back to where we were earlier this year quickly. Do we all suffer from short-term memory loss? Perhaps, as Semil pointed out above.

So lots of things are great, and lots of things aren’t great. Which way the teeter-totter swings isn’t up to us, but hot dang things are confusing at the moment.