Editor’s Morning Note: What’s the opposite of waiting for a decacorn IPO? No, it’s not practicality and good sense.

You know what pyramids have always needed? No? Watch this!

Mattermark tracked the US IPO market for technology companies closely this year—mostly with one hand over our eyes while wincing.

The scale of illiquid equity and prior investment that has been accreted under the unicorn aegis is stunning. But staggering or not, most of it remains frozen solid, waiting for favorable market conditions or the like. There are various excuses.

But while we have had a domestic focus, there is, in fact, a whole world out there past the shores of America that demands our attention.

If you can recall back to August, these pages interviewed James Clark from the London Stock Exchange about what was going on across the little lake.

To refresh your memory, here’s today key tidbit:

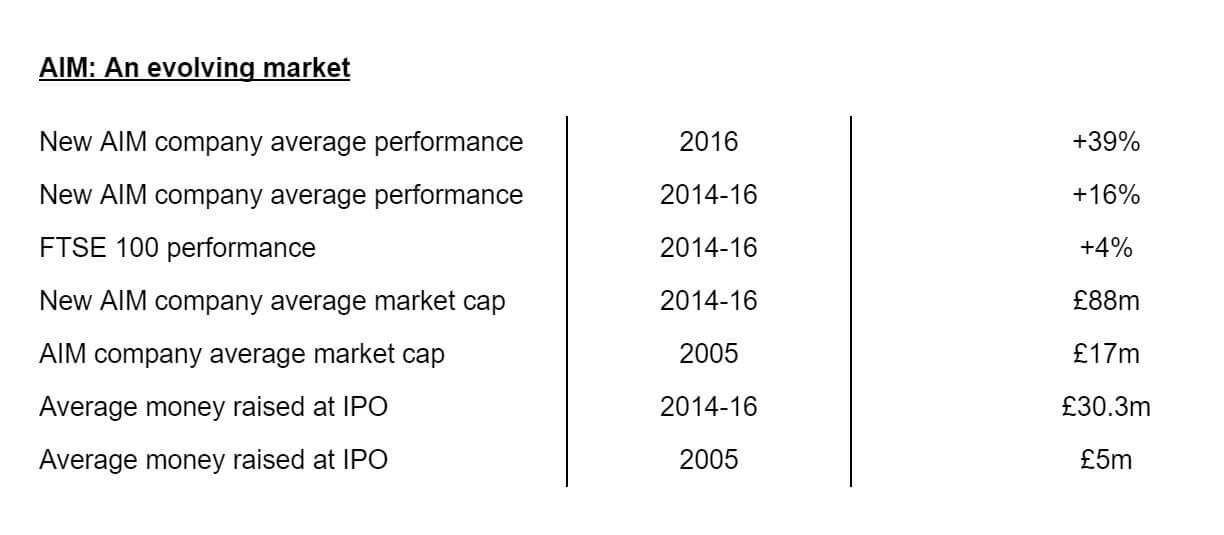

If you had forgotten that companies can go public for less than one or ten billion, I forgive you.

For our shared delectation, Clark shared a grip of new data with Mattermark concerning AIM’s performance. Let’s take a look.

Draw A Bead

Saving you from unneeded preamble, here are the new figures we have:

There are things to take from the above.

First, companies of modest cap can post healthy returns. The concept among American tech companies, our normal saw, is that most value growth should be kept to the private market does not appear to have full international translation. AIM, of course, accepts more than just tech shops.

The 39 percent figure is healthy enough, and when compared to the recent multiyear, the result looks even stronger.

That is not to say that you should take your US-based startup to London. I have no idea what you should do (and no idea, in general), but it’s good to know that there are more market options than two.

Continuing, the final two results are my favorite. An IPO raise multiplier of 6x or so in just over a decade is incredibly interesting. If you contrast the 2014-2016 market cap result with the 2014-2016 average capital raise, you can infer that these public investors are buying a material stake in the debuting firm. So this is more akin to a VC-scale cut of the firm, but in the public eye.

I’m going to drag James back in for another question session once we know more about Snap’s IPO, as I am sure that he’ll have more than a few ideas. We’re going to have a lot of fun in 2017.

—

This is our last entry of the week. Stay safe, and try to not lose your mind around family, no matter how much you don’t fit in.