tl;dr: A slow IPO market and slipping sentiment among certain investors could put high-value private tech companies’ faces in a vice.

There are more than 150 unicorns at the moment. Regardless of which data source you prefer, the number of private technology companies worth north of a billion dollars is impressive. The number of unicorns worth tens of billions is even more notable.

However, while private money has been content to fund private tech companies for longer than is perhaps historically normal, public markets have treated a number of recent offerings harshly: Box’s share price remains below its IPO price despite better-than-expected financial performance; Square went public at a discount to its last private valuation; a number of tech firms have seen their valuations fall so far that they may dip under the billion-dollar mark; companies like GoPro, Etsy have seen nearly terrifying declines in value.

It’s a fair presumption that many unicorns will eventually need more cash. It’s a common guess they will raise it from private investors and continue to eschew going public. That’s predicated on a few assumptions, including the general availability of more private money, a willingness of private investors to deploy it at an acceptable valuation, and continued pressure from public investors for profitability.

If you can grow more quickly with private cash, why not take it, in other words. And it seems, at least for now, to be a possible strategy. As Mattermark reported earlier today, Series E rounds and later are flat so far in 2016, compared to 2015, but total capital raised in those tranches fell 16 percent. Series D rounds, to continue the theme, are down 7 percent so far in 2016 compared to the year-ago two month period, and the scale of such rounds has fallen by more than $20 million apiece, on average.

Investors are still willing to deploy incredibly large checks for late-stage tech companies, but enthusiasm, as you already felt in your gut, appears to be falling.

To sum quickly: Lots of unicorns, but falling dollars. That creates something of a bottleneck. Unicorns will need more cash, but if private investors are slowing their cadence, and the IPO market is rough, where do the companies go?

It’s a question with at least one possible answer: You go public anyway, if you have to.

But can you?

The Current IPO Market In Historical Context

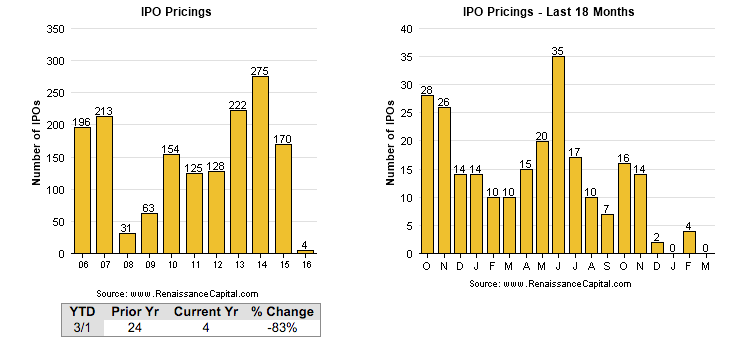

As you have heard, the current technology IPO market isn’t very strong. According to a TechCrunch report that I helped author, 2015 was the worst year for technology IPOs in terms of volume since 2009. To quote: “With just 28 technology companies entering the U.S. public markets, 2015 was the worst year for IPOs since 2009, according to Dealogic. This compares to 62 last year and 48 the year before[.]”

Keep in mind the number of unicorns compared to the number of IPOs that we have seen. The combined last three year’s IPO rate is smaller than the current number of unicorns. And that comparison becomes stiffer when you factor in that some IPOs, in fact, happen below the billion-dollar threshold; unicorn IPOs, if you will, are only a subset of reported numbers. That makes the gap between current unicorns that may eventually go public, and the rate by which the market has recently received them even greater.

Interestingly, the broader IPO market is also in rough waters. 2014 was the strongest year for American IPOs in terms of dollars raised and offerings floated since 2000, but things have changed. The current landscape is bleak [Data represents all sectors]:

An IPO Wave?

Technology IPO activity can be impressive. Mattermark reported in the past that during the 2000-era tech boom, tech IPOs managed several hundred per year for several years. Compare that to recent performance, and it’s obvious that under certain market conditions, the market will accept a huge number of technology IPOs.

However, given recent performance of newly, and recently-public technology flotations, it appears doubtful this is the case at the moment. (A fair counterargument at this point is only weaker tech shops have gone public in recent years, as stronger firms have larger access to private capital. Therefore, poor performance of recent tech IPOs is skewed by who is pulling the trigger. Even if this is true, its forward-facing meaning only holds true if similar amounts of private capital remains on offer.)

2016 has been a slow year thus far for technology IPOs. A few sample headlines: Technology ‘unicorns’ stay shy of IPOs; Tech IPO drought is sign of investor reality check; IPO Market Comes to a Standstill; Tech sector sell-off sends 2015 IPOs below issue, challenges 2016 tech.

Call me a pessimist, but I think it is fair to say a rash of tech IPOs is not pending. Also, there is a lead time to going public that many companies may have put off, presuming that they could raise another private round at an attractive valuation. If that is the case, and it must be for at least some unicorns, they could have overshot the waiting period.

According to an Ernst & Young report concerning IPOs—which itself notes that 2015 IPO volume for tech firms fell 47 percent, and that dollars raised fell 27 percent in the year—it takes “at least two years to plan” an offering. If you can’t get your IPO done in time, and you don’t want to raise capital at a lower valuation than your last, your options begin to get messy.

What I have not heard in recent months is that a large number of private tech companies are racing to go public. That combined with market data concerning pace, and the time to get an IPO into place, points to a slow 2016 for tech offerings.

Falling Valuations, A Retraction In Burn, And A Different Landscape

The current tech slowdown, as it is sometimes called after a second martini, is leading to companies pulling back on expenses. Less $10,000 bikes, for example. Cost control and burn reduction are a current theme and that means private tech companies are working to extend their cash runways. It’s prudent.

For companies that need to raise, it’s generally being said they should do so now—not later. This implies that capital could become even more scarce.

Companies that do need to raise this year could be faced with a lower valuation. As the private and public markets have struggled to agree on just what a tech company is worth, large financial institutions are marking down their holdings in unicorns. Here’s a recent report:

“One of Morgan Stanley’s mutual funds has marked down by 27 percent the value of its investment in Flipkart, a high-flying Indian e-commerce firm. The mutual fund, called the Institutional Fund Trust Mid Cap Growth Portfolio, now values its stake in Flipkart at $103.97 per share, which reflects a valuation reduction from about $15.2 billion to $11 billion for the start-up. […]

The Morgan Stanley fund reduced the value of its equity in Palantir Technologies for example, which is valued at over $20 billion, by 32% from $11.38 per share to just $7.70 per share. The fund also marked down its stake in popular file hosting service Dropbox by 25%.”

To quote the comedian, that’s bad because it’s not good.

This + That + Uh Oh

In short, if unicorns that need cash can’t raise at the valuation they want, or go public given current market conditions, we could see a host of downrounds and some deletions. But we have heard this before, haven’t we?

A refresher:

https://twitter.com/pmarca/status/515216965183754242

Welcome to 2016.