tl;dr: Here’s a primer on the language of venture capital.

Previously in Mattermark, we published a Beginner’s Guide to VC. What we neglected to include was a dictionary of jargon that insiders love to bandy about in Sand Hill Road offices.

Of course, this dictionary is not a complete representative of all the words and phrases found in legal clauses, obscure securities laws, and terms of art. But we hope this resource serves as a springboard for founders, aspiring investors, journalists, and the merely curious to learn more.

To achieve our goal, we decided to organize the dictionary thematically rather than alphabetically. (Our dictionary is a work in progress. If there are any terms that you would like to see defined, or if you have definitions of your own that might improve or add to what we have written, feel free to share them with me over email.)

A quick note: Wherever we use a definition word-for-word from authoritative written sources, we cite it using standard parenthetical style. In other cases, we’re sure to provide links and other supporting information.

The Basics

Private Equity

- Shares of a company that are not traded on a public market.

- Typically, in the United States, Private Equity investors are typically thought of as providers of capital to later stage companies.

Venture Capital

- “Independently managed, dedicated pools of capital that focus on equity or equity -linked investments in privately held, high-growth companies. […] Outside of the United States, this phrase is often used as a synonym for private equity and/or leveraged buyouts.” (Lerner, Leamon, and Hardymon 2012)

Venture Capital / Private Equity Firm

- An organization set up to manage one or more venture capital funds.

Venture Capital / Private Equity Fund

- “A pool of capital raised periodically by a private equity organization. Usually in the form of limited partnerships, private equity funds typically have a ten year life, though extensions of several years are often possible.” (Lerner, Leamon, and Hardymon 2012)

Investors Who Invest in Startups

Accredited Investor

- United States: An individual or institution who satisfies certain tests based on net worth or income as stipulated by the Investment Company Act of 1940.

Read more:

- Rules defining “accredited investors” vary from country to country. Wikipedia has a good summary of these rules in various countries.

- It is best to consult a lawyer or a national private equity or venture capital association if you are uncertain about your accredited status. A list of these VC associations can be found here.

Friends & Family

- Typically non-professional investors who provide capital to a startup company based on their close connection to a startup founder through familial, collegial, or professional relationships.

Angels

- Independently wealthy individuals who invest their own money into startup companies, usually as part of a broader investment strategy.

- So-called “Super Angels” meet the above definition but also possess exceptional insight, experience, and connections in the startup ecosystem.

Used in a sentence: “Sure, that old oil magnate makes angel investments into startups, but we’re looking for intros to super angels like Ron Conway and Scott Banister.”

Accelerator

- A program that aims to accelerate the growth of startup companies through mentorship, brokering connections, and providing services and infrastructure (such as office space) for small portions of equity in participating companies.

Seed Investor

- Institutional investors who deploy capital into very early-stage startup companies. Seed investors are considered a subset of venture capitalists.

Read More:

- Mark Suster explains the definition of a Seed vs. Series A round.

Venture Capitalist

- Institutional investors who deploy capital into private, early-stage technology companies. Venture Capitalists are usually the next group of investors to commit capital after Seed Investors.

Note: Technically, Venture Capitalists are a subset of private equity investors, but in common American usage, Venture Capitalists are considered separate from Private Equity.

Private Equity Investor

- Private Equity Investors are institutional investors who deploy relatively large amounts of capital into later-stage technology companies to fuel expansion, finance M&A activity, or to tide the company over prior to their initial public offering.

Corporate Venture Capital (CVC)

- “An initiative by a corporation to invest either in young companies outside the corporation or in business concepts originating within the corporation. These are often organized as corporate subsidiaries, not as limited partnerships.” (Lerner, Leamon, and Hardymon 2012)

Read More:

- The NVCA has an entire research page devoted to CVC.

- CB Insights published a list of the 104 most active CVC funds back in early 2015.

Investors Who Invest in Investors

Limited Partner (LP)

- “An investor into a limited partnership, such as a venture capital fund. Limited partners can monitor the partnership’s progress but cannot become involved in its day-to-day management if they are to retain limited liability.” (Lerner, Leamon, and Hardymon 2012)

Note: There are many types of investors who can become limited partners in an investment vehicle. In general, they are all considered accredited investors. Below are examples of types of investors who might invest in a venture capital fund.

Family Office

- A private advisory firm that typically manages the wealth, taxes, and estate planning of ultra-high net worth investors (i.e. individuals or families with more than $100 million in investable assets).

Pension Fund

- A pooled investment fund run by an intermediary on behalf of a government or corporation for the purpose of providing pensions to employees. Typically, pension funds deploy their assets into venture capital as part of their risk capital investment strategy.

Read More:

- Globally, long-term pension assets total some $35.4 trillion USD at the end of 2015—some 80% of annual global GDP. For more insights and information into the pension fund space, check out the 2016 Global Pension Assets Study from Willis Towers Watson.

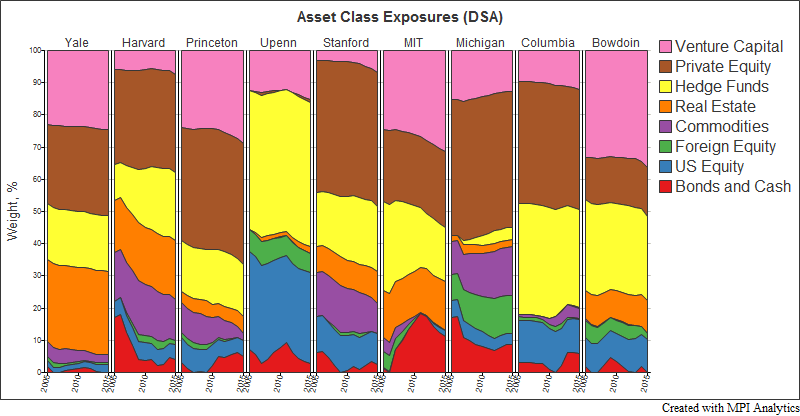

Endowment Funds

- The long-term pool of financial assets held by many universities, hospitals, foundations and other nonprofit institutions.

Read More:

Markov Processes International published a report with a visualization of the relative share of different asset classes in several top university endowments. Notice how, in all cases (with the exception of UPenn), venture capital and private equity investments account for between 25% and 50% of most university endowments between 2005 and 2015.

Funds of Funds (FoF)

- An investment vehicle that allocates its assets among a number of venture capital or private equity firms – rather than directly into private companies – on behalf of its investors.

Note: Generally, Funds of Funds serve a similar set of limited partners as regular venture capital and private equity firms. However, different Funds of Funds’ portfolios are usually designed to serve the needs of each class of investors. For example, Common Fund was set up to pool and manage the assets from smaller college endowment funds.

The Cast of Characters

Analyst

- The most junior people at a venture capital firm, usually a recent college graduate. The primary role of analysts is to network and serve as the venture firm’s “boots on the ground” in an intelligence-gathering capacity. Analysts are also tasked with performing preliminary screening, business analysis, and market research.

Read More:

- Ask Ivy had a great explanatory article on the most common roles within a VC firm. It’s referenced throughout this section.

Associate

- Associate roles are the next rung up on the hierarchy. These positions are typically “partner track” and open to applicants with graduate degrees or to analysts who’ve been working with the venture firm for a few years. Associates are usually tasked with due diligence research, obtaining progress reports from portfolio companies, and acting as the intermediary between investment prospects and the partners who make final investment decisions.

Principal / Vice President

- Principals will typically sit on a few boards of the fund’s portfolio companies and will help scout out opportunities for these companies to be acquired. The Principal position is typically the next rung on the ladder to Partner status.

Venture Partner

- “A Venture Partner is a person who a VC firm brings on board to help them do investments and manage them, but is not a full and permanent member of the partnership,” according to Fred Wilson. Venture Partners, unlike Entrepreneurs in Residence, will usually source multiple deals for the firm over the course of their tenure.

Read More:

- Fred Wilson’s post about Venture Partners is very informative.

Partner

- Partners have a similar job description to Principals and Venture Partners. They also sit on the boards of portfolio companies and spend much of their time networking. However, partners are also tasked with more high-level duties, such as identifying emerging technology sectors in which the firm will invest, identifying and developing rapport with key players in those sectors, assessing and communicating fund performance to limited partners and, every five to seven years or so, raising another fund.

VC Economics

Fund Term

- Most venture capital funds raise a finite amount of money and operate for a finite period of time. Once the target fund size has been reached, that capital is under the fund’s management, usually for a period of ten years. Fund managers usually have the option to extend the fund’s term by two to three years, often in one year increments, at their discretion.

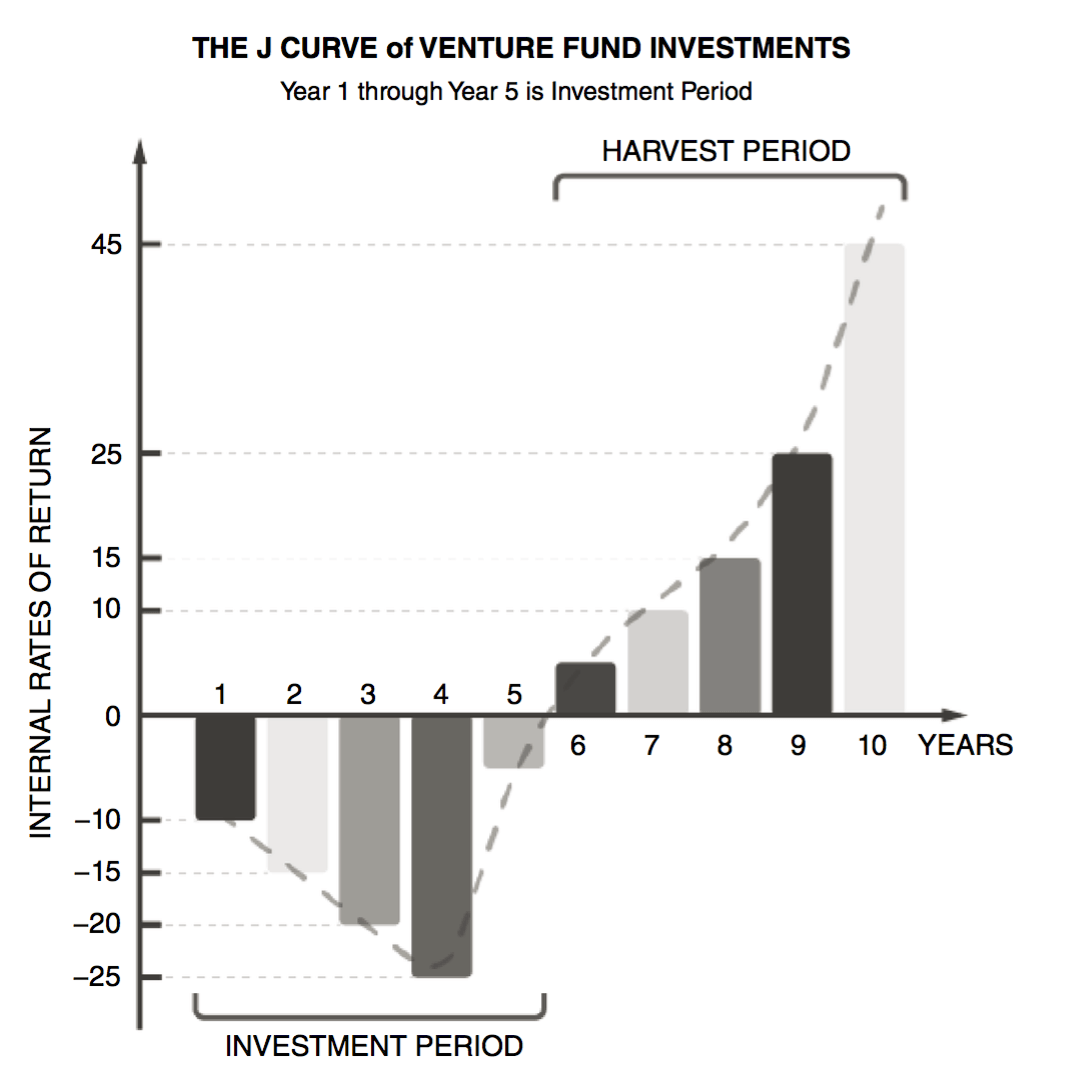

Investment Period

- The period in which the fund deploys the majority of its capital into its portfolio companies, which is typically somewhere between three and five years.

Harvest Period

- The period in which the fund begins to see returns from its investments through mergers and acquisitions, initial public offerings, technology licensing agreements, and other means.

Internal Rate of Return (IRR)

- “The annualized effective compounded return rate that can be earned on the invested capital, otherwise known as the investment’s yield. [For venture capital firms], the longer the money is tied up in an investment, the higher the multiple of the original investment that must be returned to have an adequate Internal Rate of Return.” (Lerner, Leamon, and Hardymon 2012)

Note: Ramsinghani puts a simpler spin on this: “The faster a portfolio company is sold, for as high an amount as possible, the higher the [Internal Rate of Return]. This is often where things can get tricky. A speedy exit involves selling a startup, and this can clash with the realities of market conditions and lofty entrepreneurial ideals.” (6, Ramsinghani 2014)

Read More:

- A Youtube channel with a name we can’t say in polite company published a surprisingly entertaining, informative (and mercifully short) video explaining IRR.

J-Curve

- The shape of the Internal Rate of Return curve over the course of the fund’s lifecycle, encompassing both the investment period and the harvest period.

Note: The J-Curve is so-called because it looks like a capital letter J, kind of.

Read More:

- Capital Dynamics has a good report about the VC J Curve.

Cash-on-Cash Return

- “A simplified method for calculating return by dividing the total amount of money received from an investment (or the combination of cash returned and the current value of the portfolio) by the amount initially committed.” (Lerner, Leamon, and Hardymon 2012)

- This is synonymous with the phrase, “Multiple on Invested Capital” or MOIC for short.

Example: Let’s say an investor commits $10 million to a given portfolio company. For ease, let’s also assume she does not engage in any follow on investment. The portfolio company is acquired and the investor receives $50 million in proceeds from the acquisition, meaning that the Cash-on-Cash Return (or MOIC) of the investment was 500%.

Read More:

- Macabacus published a good synopsis of the difference between Internal Rates of Return and Cash-on-Cash Returns. Macabacus also detailed the methods used for calculating each metric.

Assets Under Management

- The total market value of the financial assets which the venture capital fund manages on behalf of its limited partners.

Management Fees

- The annual fee the venture fund charges for its management services, typically 2% of assets under management, but there is some variation.

Note: The management fee is used to pay base salaries, rent, legal and other service fees, marketing costs, and other incidental expenses the fund may incur over the course of its management.

Carried Interest, or “Carry”

- The fee charged by the firm on the profits generated on a particular investment, typically 20%. This serves to align the interests of limited partners with the general partners managing the fund.

Fun etymological note: Carried interest has its origin in the 16th Century when goods were transported across the Atlantic and Pacific oceans. To pay for the ship’s expenses and compensate for the risk of the voyage, ship captains would take a customary 20% fee on the profit generated by the sale of carried goods. (Kocis 2009)

Read More:

- There are some financial technicalities around carried interest that are a bit beyond the scope of this entry. There is a surprisingly good Wikipedia article on what’s known as the “Distribution Waterfall” that provides some insights into how/when/if carried interest is disbursed to general partners in a venture capital or private equity fund.

- CalPERS, one of California’s biggest pension funds, and a major investor in venture capital, published a handy slide deck with examples of carried interest calculations.

- For a more nitty-gritty look, investment firm Duane Morris also has a good deck explaining carried interest.

- ValueWalk published some interesting data from CalPERS’s private equity performance reporting website in a small study of carried interest and fund performance.

The Art of the Deal

Financing Round

- A financing round is a type of securities offering wherein a company receives capital from investors in exchange for equity, as a loan, or in some other financial arrangement.

Note: Startup financing usually occurs in a number of rounds or stages. The standard naming scheme is to label each round with a letter from the alphabet, starting with A and incrementing up from there. But in recent times, the rise of Seed Investors has created some confusion about naming. Some refer to the money raised in a round from Seed Investors as “Series Seed” while others, such as Y Combinator, the vaunted Accelerator program, refer to these pre-Series A rounds as “Series AA.”

Lead Investor

- The principal provider of capital in a given financing round, typically the same firm from round to round.

Read More:

- Fred Wilson’s “What Exactly is a Lead Investor?”

Syndicate

- The network of investors that are also participating in a given round.

Pre-Money Valuation

- The valuation placed on a company prior to any additional investment in its current financing round.

Read More:

- Bill Payne and the Angel Capital Association wrote a digest of various methods investors use to place a valuation on early stage startup companies.

Post-Money Valuation

- “The product of the price paid per share in a financing round and the shares outstanding after the financing round. As a rule of thumb, the pre-money value plus the new money raised. This rule of thumb is true only if there are no stock redemptions or warrants issued.” (Lerner, Leamon, and Hardymon 2012)

Due Diligence

- The process of investigating a business prior to making an investment, forming a business partnership, or other long-term binding agreement.

Read More:

- The American Society of Mechanical Engineers shared a typical checklist investors might follow when undergoing due diligence research on a prospective portfolio company.

Term Sheet

- An outline of the structure of a partnership or stock purchase agreement that is typically negotiated and agreed upon before more formal language is drafted in a final binding contract.

Dilution

- “The reduction in the fraction of a company’s equity owned by the founders and existing shareholders that is associated with a new financing round.” (Lerner, Leamon, and Hardymon 2012)

Down Round

- A round in which the valuation of the company declines relative to the previous round. This might trigger anti-dilution provisions in the investment agreement.

Anti-dilution Provisions

- The financial mechanisms placed into a preferred stock agreement to maintain the investor’s percentage share in the company if the company raises a future round at a valuation lower than the one at which the preferred shareholder purchased the shares.

Note: There are several types of anti-dilution protection, but the most common among startup investment agreements is referred to as “Ratchet.”

Read More:

- Startup Company Lawyer answers the question, “What is Full Ratchet Antidilution Protection?”

Liquidation Preference

- “In a preferred stock agreement, a provision that ensures preference over common stock with respect to any dividends or payments in association with the liquidation of the company.” (Lerner, Leamon, and Hardymon 2012)

Read More:

- Learn VC’s post about Liquidation Preferences is a good resource.

Capitalization Table

- A list of investors in a startup including the names of shareholders, number of shares held, percentage ownership, and which classes of stock are owned by whom.

Warrants

- The option to buy shares of stock issued directly by the company at a certain price at some point in the future.

Convertible Note

- A kind of financial instrument that, under certain conditions specified in the investment agreement, converts from a debt owed to the investor to equity in the company owned by the investor.

Note: Convertible Notes are a common solution to the challenge of putting a valuation on the underlying company in the presence of tremendous uncertainty in very early-stage companies. That process of valuation is usually deferred to Series A investors. Once a valuation for the company is determined, the holder of the convertible note is granted the ability to convert the outstanding balance of the loan (i.e. the initial principal plus any interest accrued during the holding period) into equity in the company, proportional to the company’s valuation.

That said, the world of Convertible Notes is a bit too complicated to explain in one entry and deserves its own dictionary. For example, convertible notes may have any number of financial and legal terms attached to them, including valuation caps, discounts, and others. In lieu of explaining all of these terms, we’ve linked to some excellent resources on convertible notes:

- Startuplawyer.com’s great guide to convertible notes that comes complete with a glossary of some of the legal terms involved.

- SeedInvest’s explanation of capped versus uncapped convertible notes.

- TechCrunch‘s article “Convertible Note Seed Financings: Econ 101 for Founders.”

- Manu Kumar of K9 Ventures published his Thoughts on Convertible Notes.

- Gust Equity Management made an interactive convertible note calculator.

SAFE Note

- An abbreviation for “simple agreement for future equity,” this financial instrument closely resembles a convertible note, except they are not a debt instrument.

Read More:

- Y Combinator was the first to implement the SAFE note and has an explanation on their site. They also have sample SAFE agreements and a very detailed “SAFE Primer” that maps out multiple investment scenarios for SAFE holders.

Bibliography

Brad Feld and Jason Mendelson, Venture Deals: Be Smarter than Your Lawyer and Venture Capitalist, 2nd ed (Hoboken, N.J: Wiley, 2013).

James M. Kocis, ed., Inside Private Equity: The Professional Investor’s Handbook, Wiley Finance Series (Hoboken, N.J: Wiley, 2009).

Joshua Lerner, Ann Leamon, and G. Felda Hardymon, Venture Capital, Private Equity, and the Financing of Entrepreneurship: The Power of Active Investing (Hoboken, NJ: John Wiley & Sons, 2012).

Mahendra Ramsinghani, The Business of Venture Capital: Insights from Leading Practitioners on the Art of Raising a Fund, Deal Structuring, Value Creation, and Exit Strategies, Second edition, The Wiley Finance Series (Hoboken, New Jersey: Wiley, 2014).