If you had hoped for a relaxed Monday, you lose: Microsoft will buy LinkedIn in a surprising deal worth more than $25 billion, Apple’s WWDC keynote kicks off shortly, Twitter shares are actually up, and there is something games-related going on as well.

Get another coffee.

Microsoft Buys LinkedIn At A Discount

Microsoft will purchase LinkedIn for $196 per share, or $26.2 billion. The deal came a shock to the technology community, at least so far as I can tell. Its announcement comes directly before Apple’s widely anticipated keynote.

The deal sent Microsoft’s shares off a few points, while LinkedIn’s equity shot north to, surprise, the $190 range. The difference between the $196 per-share deal value and LinkedIn’s $192 current price is likely a form of risk spread, if you want to think of it in that way.

What’s notable, but easy to miss in the deal is that Microsoft is buying LinkedIn at a discount. The company traded as high as $258 inside of its 52 week range. So, Microsoft, even after paying a massive premium for the company — around 50 percent — is still purchasing the firm at a lower price than the public markets were perviously and recently content with.

As you will recall, LinkedIn took a whacking earlier this year following a lackluster earnings report. Slowing user growth, and missed guidance led to a double-digit kneecapping of its value. Microsoft, therefore, is buying LinkedIn at a premium to its reset valuation. So it’s a win, but.

What in the flying hell will Microsoft do with LinkedIn? Boil me in soup if I understand the play, but here’s a important question: How accretive will LinkedIn be to Microsoft’s top line? LinkedIn’s last quarter saw it bring in revenue of $861 million. Microsoft’s Surface business alone did over $1.1 billion during the corresponding period1.

Given that, the LinkedIn deal cannot be about short-term financial gain. It must concern driving usage across Office 365. If that works, helping Microsoft build recurring revenue is a big, open question.

The Best Private Companies, Or One Of The Best Public Companies?

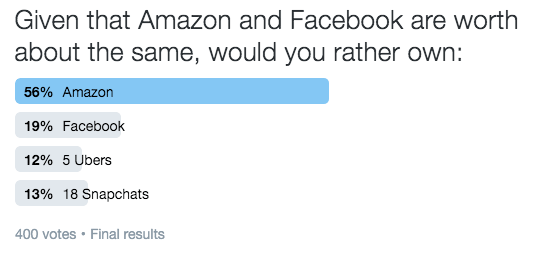

Returning to private companies, I ran a bit of a poll over the weekend asking if people would rather own a collection of Uber or Snapchat-valued unicorns, or just Facebook or just Amazon. The question was predicated on the fact that Facebook and Amazon have very similar market capitalizations, and Uber and Snapchat are two of the most respected private technology companies.

You could get your hands on around 5 Ubers or 18 Snapchats for the same price as one Amazon or one Facebook. As such, I expected that startup kids and investors would flock towards the high-growth, if unprofitable Uber and Snapchat poll options.

Here are the results:

Boo, optimism, apparently.

Two things that stand out: Snapchat beating Uber regardless of caveats is a surprise. Also notable is the margin of victory that Amazon managed over Facebook. In short, voters were more bullish on Amazon than Facebook, 5 Ubers, or 18 Snapchats combined. Of course, all this valuation math is difficult to fully set into place, given that our public companies trade every day, while our private firms reprice less frequently.

You could read that chart as individuals finding themselves more bullish about proven companies than startups, but by reaching that potential conclusion we are stretching into Trelawney’s domain.

—

I could bang on but that would preclude you from Googling ‘WWDC livestream’ and giving another publication a pageview. Off you go!

- Surface revenue data here. LinkedIn revenue data here. Not only did Surface have more revenue than LinkedIn in the last quarter, if you rewind a bit, the trend is equally obvious.