tl;dr Investors pre-paid too much for expected future growth.

Taking a break from our usual focus on markets and not individual participants, let’s dig into what in the heck is going on at LinkedIn. The company’s shares are down roughly 25 percent today in late trading after reporting strong fourth quarter earnings.

If that makes little or no sense, don’t worry. We’ll get there. First up, let’s see how the company did compared to investor expectations in the fourth quarter.

Expectations:

- Revenue: $857.6 million

- Adjusted per-share profit: $0.78

Results:

- Revenue: $861.9 million

- Adjusted per-share profit: $0.94

That’s a solid beat. LinkedIn brought in more money than expected, and also managed to hold onto more dollars during the financial period than investors anticipated. But every quarterly report is a look in reverse, meaning that forward guidance can sometimes be the larger story.

This is one of those times.

What Have You Done For Me Lately

LinkedIn reported a solid fourth quarter, but in the same breath — its earnings release — told the markets its expectations for its first quarter, and full year. Here’s what the market expected for the first quarter of 2016, prior to the company’s fourth quarter 2015 results:

- First quarter revenue: $866.86 million

- First quarter adjusted per-share profit: $0.74

- 2016 revenue: $3.91 billion

- 2016 adjusted per-share profit: $3.67

Those figures, if met, would have included a roughly $1 billion increase in revenue for LinkedIn during the year, and just under $1 more in per-share profit, employing adjusted metrics. LinkedIn lost money in its fourth quarter using normal accounting techniques, but as investors currently grade the company more on its adjusted figures, that’s where our focus rests.

Here’s what the company indicated it will deliver in the current calendar year:

- First quarter revenue: $820 million

- First quarter adjusted per-share profit: $0.55

- 2016 revenue: $3.6 billion to $3.65 billion

- 2016 adjusted per-share profit: $3.05 to $3.20

You will note that the second set of figures is smaller. LinkedIn is projecting growth in its top and bottom line, but less than market expected.

Your Beat Is My Miss

Given the discrepancy between the company’s own guidance, and expectations it isn’t hard to see why investors are at least a bit disappointed. But is a 25 percent drop warranted? You might think not.

It’s a question of future growth. Investors who owned LinkedIn expected the company to generate larger future cashflows than it itself anticipates. That is the opposite of bullish. You can run your own discounted cashflow analysis, but less revenue means not good. Roughly.

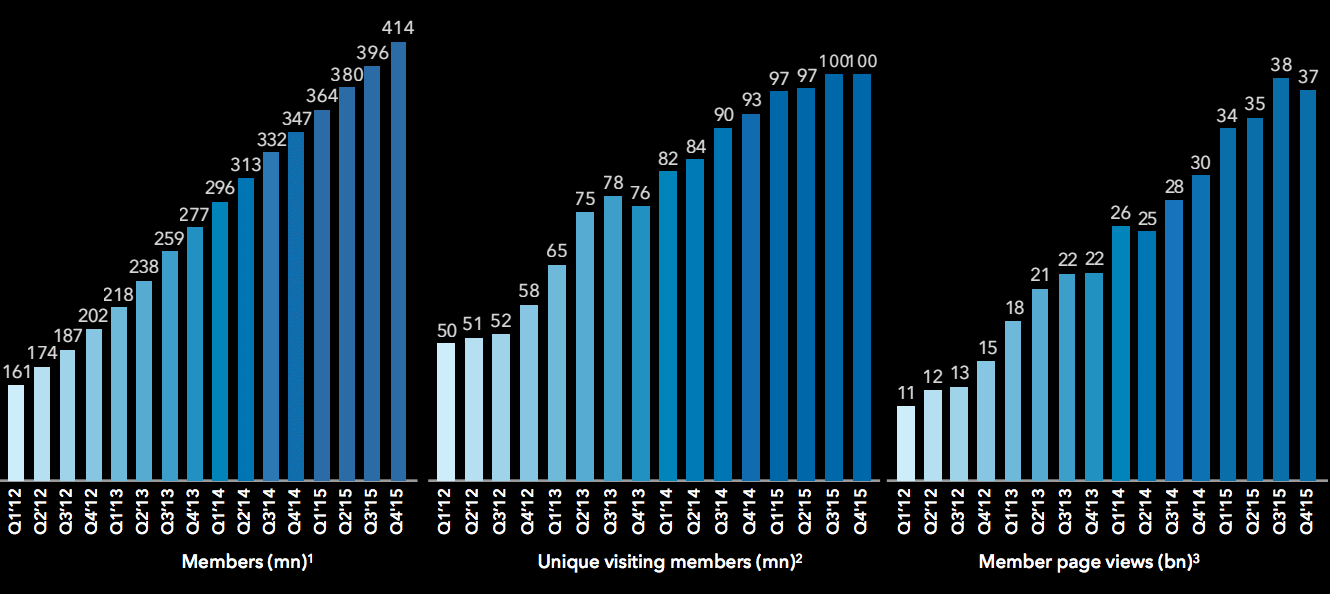

LinkedIn also managed to tie in another negative moment to the quarter. Look at the following chart, released as part of its fourth quarter earnings package:

Two of those charts are flat or down. That’s not so good. Call it the Twitter problem, if you want: Growing financial performance coupled to slowing user metrics. This ties back to growth. A company that depends on users to monetize needs more of them over time. Slowing unique visitor growth, for example, could indicate that future revenues tied to that portion of the LinkedIn business will generate lowers incomes in the quarters to come.

It’s bad, in other words.

LinkedIn’s morning trading session will be interesting.