Editor’s Morning Note: After publishing our post looking ahead to a quickening tech IPO cadence, Coupa filed. Let’s investigate.

There are now enough US-based tech IPOs that it’s easy to forget one or another. Nutanix, The Trade Desk, PointClickCare, and Apptio are now joined by Coupa, a company that helps other firms with spend management.

Coupa is growing quickly and has managed to freeze its losses. In fact, during the first six months of 2016, its losses fell slightly while its revenue grew by eight figures.

How well, or poorly, is Coupa set to do when it embarks into the public markets? Let’s do our best to find out.

Your Valuation, Our Wager

As everyone noted in the immediate aftermath of the Coupa filing, the company is a unicorn, having been awarded a valuation of $1 billion or more from investors. There are more than a dozen dozen unicorns in the world today, making Coupa decidedly un-rare1 in that regard.

However, a unicorn going public is damn rare. That’s why we care.

Now, what is Coupa worth? As BusinessInsider notes, the company raised $169 million as a private company, of which it holds tens of millions in cash. But that is looking backwards. What will the company be worth when it first sets its IPO range, then formally prices, then opens, and then closes after its first day?

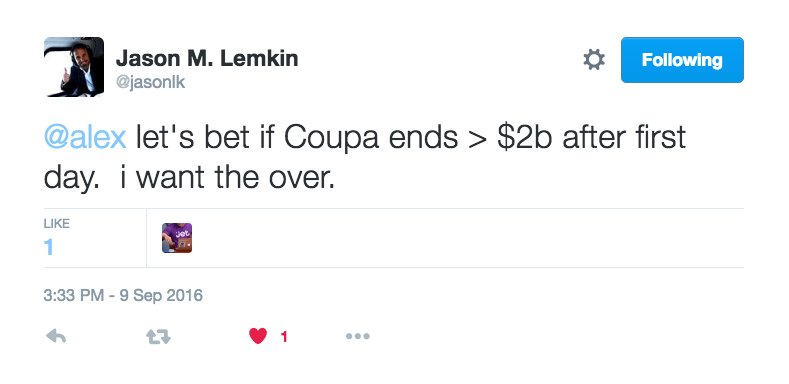

Well, we have at least one vote on the record:

Fair enough. I didn’t take the under; I lack enough information to make the bet, at least for now.

Multiples And Historical Context

How might we value Coupa? We can use a few multiples to make educated guesses, but let’s get some raw numbers in front of our noses.

We’ll kick off with revenue:

- Most recent quarter’s revenue: $31.13 million.

- Sequentially preceding quarter’s revenue: $29.18 million.

- Revenue growth, measured from its sequentially preceding quarter: 6.68 percent.

- Year-ago quarter’s revenue: $18.70 million.

- Revenue growth, measured from year-ago quarter: 83.36 percent.

This all feels quite positive. The company’s subscription-heavy revenue is growing quickly. The company could have expanded more rapidly, I suppose. But I think the market will be content with those figures.

Next up, profit:

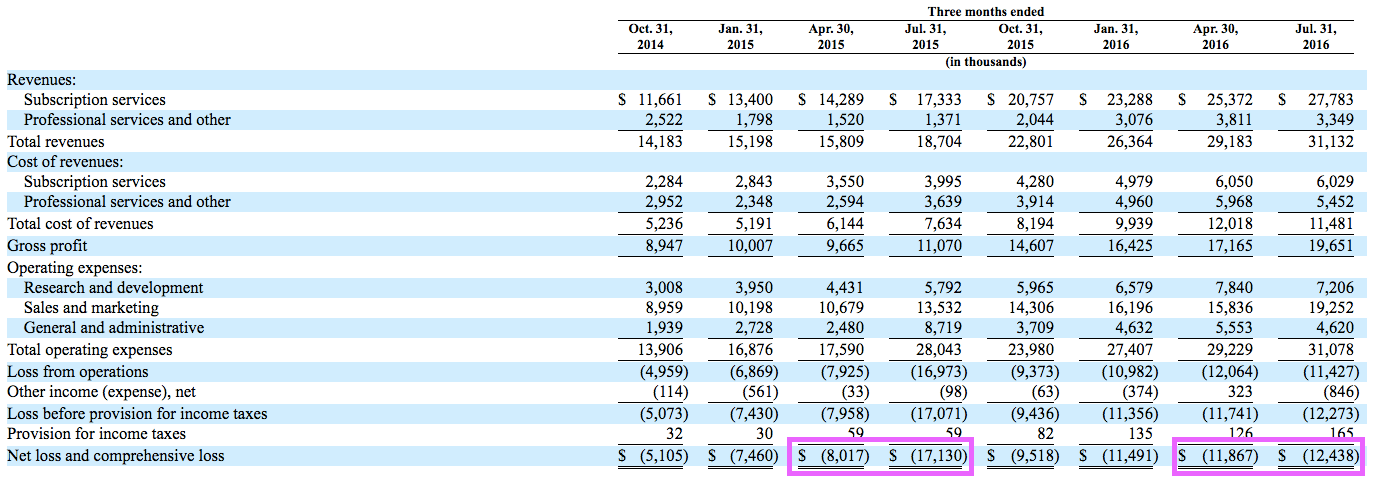

- Most recent quarter’s gross profit: $19.65 million.

- Most recent quarter’s net income: -$12.44 million.

- Year-ago quarter’s gross profit: $11.07 million.

- Year-ago quarter’s net income: -$17.13 million

This is a bit more modest. The large increase in gross profit is solid, and it is roughly in-line with its revenue expansion over the same time period, The company’s gross profit, however, grew millions more in dollar-terms than the company’s net loss contracted.

Recall our prior note that “during the first six months of 2016, [Coupa’s] losses fell slightly while its revenue grew by eight figures.” It’s nearly silly how that truth works out. Observe the glory of lumpy mid-stage earnings:

In Coupa’s two most recent quarters, the company has seen consistent, yet-growing losses. But when you compare the two half-year periods, things have gotten a touch better in aggregate. Due to the variance in the two year-ago quarters, Coupa’s net loss decline looks far better than it did a quarter before, comparing that period to its analog.

In short, because the company had such uneven losses in the preceding year, its first quarter look as abysmal in terms of profit as its most recent quarter appears salubrious.

And cash and its enemies:

- $79.94 million in cash and equivalents at the end of the July 31 quarter.

So that’s all of that: Quick revenue growth, slipping year-over-year half-year losses, and a several quarters of operational losses in cash.

What is it worth? Sadly, our recent valuation multiple work deals with enterprise value. We can’t suss that out until the company can be properly priced, putting us in a pickle. Although, if we take a few quick ratios from prior work, we might be able to get a range in mind.

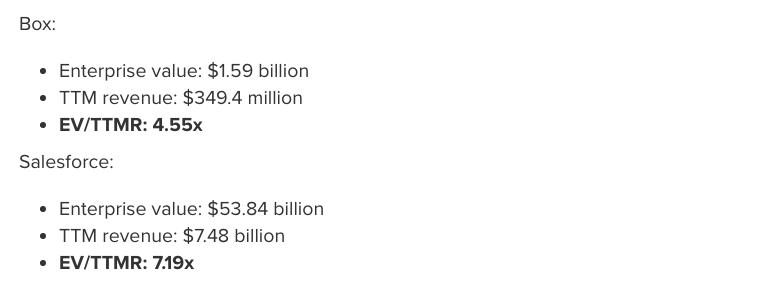

From our piece, The Changing Value of ARR IV, we learned the two ratios at which Box and Salesforce trade. Apologies for the quote:

All we need is Coupa’s trailing twelve month (TTM) revenue, and we can do some doodling:

- Coupa’s TTM revenue: $109.48 million2.

- Coupa’s value using Box’s EV/TTMR ratio: $498.13 million.

- Coupa’s value using Salesforce’s EV/TTMR ratio: $787.16 million.

The math isn’t great. We are using EV ratios when, for now, we shouldn’t. That means the above figures are inherently conservative. There are some additional caveats: Coupa’s growth far surpasses Salesforce’s on a percentage basis. As such, it may be able to command a higher multiple. Add that into an EV calculation that will shift the baseline of the ratio, and it isn’t hard to imagine the company snagging a valuation comfortably north of $1 billion.

—

I can’t say if Coupa is worth $2 billion or more, either at open or close of its first day, but it does seem fair that Coupa has a pretty clear path to its offering (provided that it doesn’t price itself out of a flotation).

That’s enough to start with. The rest of the S-1 is illustrative.

- No, this does not mean you can order your steak well-done. You fascist.

- Presumably, the company will update its S-1 with another quarter’s information before it goes public. We are looking at data that is a bit laggish.