tl;dr: After a strong start to the year, closer examination of the data shows that venture activity for U.S.-based companies is cooling in the second quarter. Here’s where things are, best and worst, broken out by funding stage.

Disregard text, observe arc.

It’s been 4 months since the February 5th stock market swoon solidified fears common among founders and investors alike: private valuations and their public market comps were stubbornly distant.

Since that period of temporary panic, the S&P 500 has recovered and approached record highs, the Nasdaq is back around 5,000, and Twilio has filed to go public. Good news aside, however, recent data indicates that investors have remained cautious, stuck in a “wait and see” mode through the first months of the second quarter.

As it is widely known, there is lag between when a company completes a raise, and when it announces its new round of capital. That gap can stretch anywhere from 6 to 12 weeks. Some rounds announced in the first quarter of this year, for example, were inked in the last quarter of 2015, implying that they were not influenced by the more immediately apparent sentiment found on VC blogs, Twitter, and in bars and boardrooms throughout Silicon Valley.

In this analysis, we review trends in this year’s venture capital funding for U.S. startups through May 31st in terms of numbers of deals, capital deployed, and average round sizes.

The Big Picture

In the first 3 months of 2016, deal volume rose 36 percent while capital deployment fell 3 percent. In this quarter, a total of 1,007 deals were announced by U.S. companies, raising a total of $15 billion1. Those figures compare favorably to 742 deals totaling $15.5 billion recorded in the same period last year.

While the first quarter of the year started out with strong activity levels, 2016 through May 31st shows that deal volume growth has slowed to just an 11 percent year-over-year increase. Cumulative capital deployment has fallen further, now down 8 percent year-to-date versus the same period in 2015.

Looking more granularly at the last two full months of the second quarter, April 2016 saw a 22% year-over-year decrease in the number of rounds and 30 percent decline in capital deployment, with 236 deals totaling $3.1 billion announced versus 302 deals totaling $4.5 billion in April last year.

May 2016 saw a 20 percent year-over-year decrease in the number of rounds and a 1.4 percent decrease in capital deployed, compared to May 2015. In May of 2016, there were 202 rounds totaling $5 billion, versus 254 rounds totaling $5.1 billion in May 2015.

To sum, the first quarter of 2016 was generally strong, while the first 66 percent of the second quarter is bringing the year back down to earth.

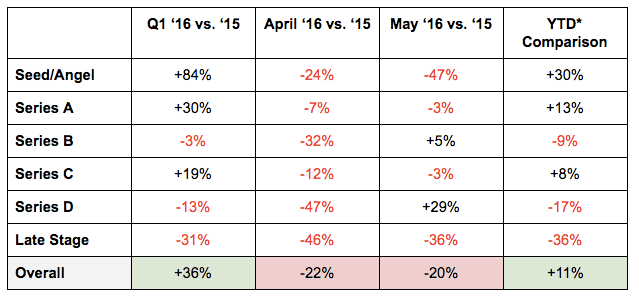

Stage-by-Stage Change in Venture Capital Deal Volume

*YTD comparison includes data from rounds announced January 1, 2015 to May 31, 2015 vs. January 1, 2016 to May 31, 2016.

This chart is a feel of the pulse of venture capital in the United States, measured on a deal basis. Notably, only late stage investments managed to decline in each measured period, while every other Series class fell in at least two of the three.

The second quarter so far is doing quick work at erasing gains notched in the first quarter.

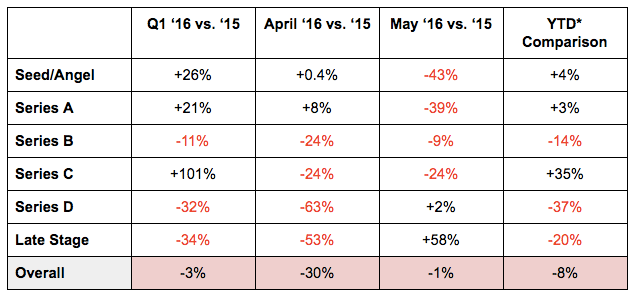

Stage-by-Stage Change in Venture Capital Deployed

*YTD comparison includes data from rounds announced January 1, 2015 to May 31, 2015 vs. January 1, 2016 to May 31, 2016.

While the first chart measuring deal flow managed some positive news, you’ll note that its largest single-period growth came from early stage investments in the first quarter. Those are smaller-dollar deals. The above, second chart shows aggregate dollars invested across each Series class for United States-based companies.

The first quarter managed a near UNCH in the first quarter, but by the end of May, things were a bit deeper in the red.

Seed & Angel

tl;dr: Things started off with a bang, but Q2 isn’t looking great.

The first 3 months of pre-Series A activity this year dramatically outpaced January, February, and March of 2015, with deal volume up 84 percent and capital deployment up 26 percent. Q1 2016 saw 460 financings announced totaling $489 million, versus 251 deals totaling $387 million for the same period of 2015.

In 2016 through May 31st, however, deal volume growth is a far slower 30 percent year-over-year increase. And that increase summed to just a 4 percent year-to-date increase compared to the same period of 2015.

- April itself saw a 24 percent year-over-year decrease in the number of angel and seed rounds, coupled to flat capital deployment at the stage. A total of 78 financings totaling $140 million took place in the month, versus 103 rounds totaling $140 million in the comparable year-ago period. At the same time, average round size grew to $1.8 million in April, up from its year-ago average of $1.4 million. Over the same timeframe, median round size doubled from $1 million in April of 2015, to $2 million in April of 2016.

Those changes may indicate that even early-stage investors are searching for “safer” investments, consolidating their focus on a smaller set of companies and investing more per deal.

- May deepened the seed stage slowdown trend, with a 47 percent year-over-year decrease in the number of angel and seed rounds, and a 43 percent year-over-year decline in total dollars allocated. In May, there were 56 pre-Series A financings announced totaling $101 million, versus 105 financings totaling $176 million in May 2015. The average round size was $1.8 million in May, and the median also came to $1.8 million.

Both deal volumes and capital deployment have decreased together, while round sizes have remained fairly constant, suggesting valuation compression at this stage is minimal. But the bar for getting funding at all has been raised significantly in the past couple months.

Series A

tl;dr: Total rounds and dollars invested are up, but May brought some big red flags.

Series A venture capital deal volume in the first 3 months of the year outpaced Q1 2015 by 30 percent, with 262 deals announced in U.S. totaling $2.3 billion versus 201 deals totaling $1.9 billion in the same period of 2015.

Average round sizes peaked in Q1, reaching $10.4 million in January before dropping to $6.7 million at the end of Q1 2016 versus $7.9 million for the same period last year. Overall, year-to-date comparisons for the first 5 months of 2016 versus the same period of 2015 show a 15 percent increase in deal volume and 3 percent increase in capital deployment.

- April saw a 7 percent year-over-year decrease in the number of rounds and 8 percent increase in capital deployment at this stage, announcing 81 new Series A rounds totaling $729 million in April 2016 versus 87 Series A rounds totaling $673 million in April 2015.

- May saw a 3 percent year-over-year decline in the number of rounds paired with an astonishing 40 percent decrease in capital deployed, with 60 Series A financings announced totaling $556 million in May 2016 versus 62 financings totaling $916 million in the same month last year.

While deal volumes are falling more gradually, the sharp decline in capital deployment indicates compression on valuations as much as 30-40 percent in some deals. The average Series A round size dropped from $14.8 million in May 2015 to $9.3 million in May 2016. For companies who raised large amounts of money in their seed rounds on notes with high caps and/or aggressive discounts, the conversion to Series A may lead to far more dilution than planned.

Series B

tl;dr: Fewer deals, less total investment, and falling round sizes make for a rough mix.

Series B venture capital deal volume in the first 3 months of the year lagged Q1 2015 by 3 percent while capital deployment fell 11 percent, with 136 deals announced totaling $2.7 billion this year versus 140 deals totaling $3 billion in Q1 2015.

Overall, 2016 cumulative year-to-date (through May 31st) funding announcements saw a 9 percent decrease in Series B deal volume and 14 percent decrease in capital deployment, with 215 rounds totaling $4.4 billion so far in 2016 versus 235 deals totaling $5.2 billion for the same period last year.

- April saw a 32 percent year-over-year decrease in the number of rounds and 24 percent decline in capital deployment at this stage, announcing 39 rounds totaling $1.05 billion in 2016 versus 57 rounds totaling $1.4 billion in April 2015.

- May saw a 5 percent year-over-year increase in the number of Series B rounds but a 9 percent decline in capital deployment at this stage, announcing 40 rounds totaling $687 million in 2016 versus 38 rounds totaling $752 million in May 2015. The average Series B round size in May was $17.2 million, down 13 percent from $19.8 million a year ago. The median round size was $14.5 million, down from $14.8 million a year ago.

Series C

tl;dr: Total investment is sharply up, but deal volume is nearly flat as Series C cool as Q2 continues.

Series C venture capital deal volume in the first 3 months of the year outpaced Q1 2015 by 19 percent, with 86 deals announced totaling $4.1 billion versus 72 deals totaling $2 billion in the same period last year.

Year-to-date Series C rounds are on the upswing. Round volume is up 8% and capital deployment up 35 percent. However, this trend was primarily driven by announcements in the first quarter, and the trend of the past 2 months indicates a significant change in the dynamics at this stage. Two more months at May’s current pace would put 2016 flat with the previous year.

- April saw a 12 percent year-over-year decrease in the number of rounds and 24 percent decline in capital deployment at this stage, with 22 rounds announced totaling $521 million versus 25 rounds totaling $684 million in April last year.

- May saw a 3 percent year-over-year decrease in the number of rounds and 24 percent decline in capital deployment at this stage, with 30 Series C rounds announced totaling $1.2 billion versus 31 rounds totaling $1.6 billion in May 2015.

Monthly average deal sizes for Series C peaked in February 2016 at $79.4 million, driven by mega rounds for Magic Leap and Oscar. However, May 2016 average Series C deal sizes declined 21 percent to $40.6 million versus $51.4 million in May last year. The median Series C round size for May 2016 was $23.8 million, with larger rounds in Pivotal ($253 million), Clover Health ($160 million), Via Transportation ($100 million), and Musical.ly ($100 million) contributing to a upwardly skewed average.

Series D

tl;dr: Fewer deals and fewer dollars, but there are still big checks available to the right companies.

Series D venture capital deal volume in the first 3 months of the year lagged Q1 2015, with 40 deals announced totaling $1.4 billion versus 46 deals totaling $2 billion in the same period last year. Overall, 2016 year-to-date through May 31st shows a 19 percent year-over-year decrease in the cumulative number of rounds year-to-date, and a 39 percent decline in cumulative capital deployed year-to-date versus the same period in 2015.

- April saw a 47% year-over-year decrease in the number of rounds, with 9 Series D rounds announced totaling $289 million versus 17 rounds totaling $781 million in April 2015.

- May saw a 14% year-over-year increase in the number of rounds and 12% decline in capital deployed versus May 2015. In May, there were 8 Series D rounds totaling $209 million versus 7 Series D rounds totaling $238 million in May 2015 (this was a slow month in 2015 relative to April and June, which saw 17 and 16 deals respectively). May 2016 average Series D round sizes are down 23% to $26.1 million versus $33.9 million in May last year. The median Series D round sizes for May 2016 was $23.5 million, with the largest round of $45 million invested in Atlanta-based Ionic Security by Goldman Sachs, Amazon, and Hayman Capital.

Monthly average deal sizes for Series D peaked in June 2014 at $132.3 million, which was skewed by a $1.2 billion mega round for Uber. The overall median Series D round size for 2016 stands at $35 million, with mega rounds including $130 million to Domo, and $100 million apiece to Guardant Health, Snagajob, and Affirm.

Late Stage (Series E, F, G, etc.)

tl;dr: So far, 2016 is no 2015 for the super late stage.

Late stage venture capital deal volume in the first 3 months of the year lagged Q1 2015, with 23 deals announced totaling $4.2 billion versus 32 deals totaling $6.1 billion in the same period last year. Overall, 2016 year-to-date through May 31st shows a 36 percent year-over-year decrease in the cumulative number of rounds year-to-date, and a 20 percent decline in cumulative capital deployed year-to-date versus the same period in 2015.

- April 2016 saw a 46 percent year-over-year decrease in the number of rounds, with 7 late stage deals totaling $372 million announced versus 13 deals totaling $793 million in April last year.

- May 2016 saw a 36 percent year-over-year decrease in the number of rounds, and 58 percent increase in capital deployed versus May 2015. In May there were 7 late stage rounds totaling $2.2 billion, versus 11 late stage rounds totaling $1.4 billion in May 2015. May 2016 average late stage round sizes are up 149 percent to $312 million versus $126 million in May last year; however, the numbers are skewed by one very large deal among a set of just 7 transactions.

Monthly average deal sizes for late stage rounds peaked in February 2015 at $334.5 million, driven higher by a $2.8 billion mega round for Uber, and 16 other rounds of $50 million or more. The median Series D round sizes for May 2016 was $75 million, with the largest round of $1.4 billion invested in Snapchat by Sequoia Capital, T. Rowe Price, General Atlantic, Lone Pine Capital, Fidelity Investments, Coatue Management, Institutional Venture Partners (IVP), and Glade Brook Capital Partners.

In Total

When the second quarter comes to a close and all the data is collected, we’ll update all the above figures to provide a more concrete year-on-year and sequential quarter analysis of venture capital trends.

For now, there is more red ink in the second quarter than the first, and if current trends hold, gains made in the first quarter could be erased entirely by a more difficult second quarter; if second quarter trends persist into the third quarter, the year will likely manage both a decline in deals and dollars invested. Currently, the score on that count is one apiece.

- Investments made by private equity firms were excluded from this study.

Join thousands of business professionals reading the Mattermark Daily newsletter. A daily digest of timely, must-read posts by investors and operators.

Gifs Via Giphy