Editor’s Morning Note: Things outside of tech are pretty big too.

The Jet.com purchase is now official, with Walmart announcing a grip of details concerning the transaction, including its final price: Around $3 billion in cash and $300 million in shares.

The shares and part of the cash will be paid out over time—likely to ensure employee retention following the deal’s closing. Today, we’ll leave operational questions to other, better qualified publications. Instead, we’ll focus on how Jet fits into Walmart’s own economic outlook. After all, $3.3 billion is big news for the world of startups, but it doesn’t necessarily mean that Walmart is breaking a sweat.

Walmart By The Numbers

Compared to Jet, Walmart towers. According to its most-recent earnings report, Walmart had the following quarterly vital signs:

- Revenue: $115.9 billion

- Net income: $3.1 billion

- Free cash flow: $4.0 billion

- Dividend payout: $1.6 billion

Those are big numbers. Huge, even.

What is all of that worth? Walmart’s market cap currently weighs in at around $228 billion. That means Walmart is trading for around half its current annual sales pace, measured using the most recent quarter—the first of its fiscal 2017—and taking it out another three.

Forget revenue multipliers, in offline retail you get a revenue divisor.

That’s in contrast to Jet, which is selling itself for a multiple of its gross merchandise volume of around 3. It depends on how you count. Jet recently disclosed that it had reached a $1.1 billion gross merchandise volume run rate, but in Walmart’s official notes, a $1 billion figure was used. Adding to the compounding is our repeated mantra that gross merchandise volume is not net revenue, which makes the ratio even richer.

Regardless, I don’t see many people crying yet over the deal from the startup’s side of things.

Ecommerce By Itself

If you root around just a bit on Walmart’s investor relations website, you can find an infographic of its earnings report which, given that it’s the morning, I read. The following stood out:

That’s not adjusting for changes in currency value, in case the faux-asterisk threw you off. On an adjusted basis, Walmart managed a 700 basis point change in its ecommerce revenue. That’s not wildly encouraging. And therein lies the chance for the Jet team to change things for the better.

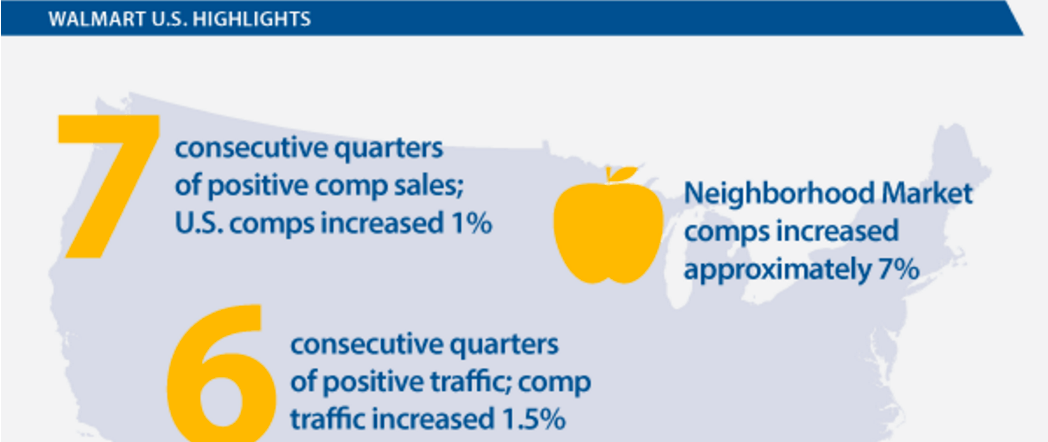

How hard is it to be a physical retailer? Check the following metrics from the same source, detailing various Walmart growth metrics:

I clipped the boring parts out, of course, but imagine calling a single percentage point of sequential growth a highlight in Silicon Valley.

The lack of growth is where Jet can presumably create impact. Walmart’s base is already large, and it has failed on its own to create a significant ecommerce presence. Perhaps Jet’s technology team can leverage Walmart’s foundation in a way that it couldn’t match alone either, thus allowing both Jet and Walmart to grow in tandem.

That is what initially confused me: Why would Walmart pay so much for something so small? Instead, the deal seems to be a very, very expensive purchase of technology and talent. For a company like Walmart, it’s a bold bet, if the scale of its cost wasn’t so small compared to its other financial metrics.

Jet is small, but Walmart’s physical growth is minute. If the Jet crew can bolster Walmart’s digital commerce business by even a few percentage points per year, you can make the math pencil out I’d hazard.

Will It Work?

As someone actively not paid to make billion dollar decisions of any variety, I am certainly no expert. But 2007 taught me something about crowdsourcing, so here’s a mirror on you1:

Put another way, the chance of Jet’s success is currently matching Trump’s poll numbers. That’s more positive than I expected.

- Read: People on Twitter yesterday who answered my unscientific poll.