Micro VC is a quickly growing category. When I began angel investing nearly a decade ago, I knew perhaps two firms. When we started Urban.Us two years go, we began discovering quite a few more. As we talk with investors and startups, we’re routinely asked everything from “what is micro VC?” to “how are firms differentiating?”. Here are some of our responses.

1. What is a micro VC?

Micro VCs are a relatively recent phenomenon in the private equity ecosystem, though some of the best-performing firms, like SV Angel, have been thriving since the 90s. They differ from traditional VCs in some important ways, beginning with the amount of capital they allocate. While micro VC firms have raised or are raising less than $100MM in funds, it is not unusual for VC fund sizes to top $1b.

Most (around 80 percent) of the initial investments that micro VC firms make are in companies that are at the seed stage, whereas traditional VCs tend to focus on later or across multiple stages. Because of the earlier stage and smaller fund sizes, micro VC funds can generate good returns relative to their venture peers, without relying on a single massive winner to generate all of the fund returns (source: Samir Kaji).

Figure: The seed stage is typified by a search for the right product and customers. This is the stage of most interest for micro VCs. The early stage remains the domain of traditional VCs, but they also invest in the late stage alongside traditional PE investors. Source: Urban.Us & Wikipedia.

Micro VCs identify opportunities at the seed stage and use various approaches to help teams escape the “Valley of Death.” There is certainly competition among funds, but micro VCs typically participate alongside other funds and angels. And some of the most successful investors have contributed to an open body of knowledge about ways to increase the chances of success through insightful essays, blog posts, Q&As and AMAs.

2. What’s contributed to the rise of micro VCs?

Returns from early-stage investments have attracted attention, and low capital requirements (for startups and funds) mean that there is more room to experiment

Data about fund performance is reaching a broader audience, too. A 2012 Kauffman Foundation report on two decades of VC investing suggests that small venture funds were the most likely to succeed moving forward. A more recent analysis by Cambridge Associates seems to confirm the Kauffman hypothesis and goes further. They found that new and emerging fund managers accounted for 40% to 70% of value creation in top-100 deals in the last 10 years.

It used to be that the micro VC was the domain of seasoned fund investors like Venture Investment Associates. Early on, they identified some of the best-performing micro VCs, like First Round Capital. Because of the broader awareness of relatively smaller commitment sizes and higher potential returns, more potential LPs are looking at the category as a way to get exposure to venture capital. It probably helps that the larger firms like Sequoia or a16z are just not accessible for most LPs.

Over the last decade, the low startup capital requirements have meant a similarly lower capital requirement for funds, so early-stage investing has seen a lot of process innovation. Funds have found new ways to leverage the same tools that their portfolio companies use for efficient distribution. From content marketing to internal communities, funds have found new ways to help attract deal flow and enable founders to connect with other founders to help de-risk their own companies.

The more noticeable changes are accelerator programs such as YC, Techstars, 500 and Seedcamp. More recently, these programs have been joined by more focused accelerators covering areas from healthcare to hardware. Similarly, crowdfunding platforms like Angel.co, Crowdfunder or Ourcrowd have increased efficiency for angel investors looking for deals and co-investors. Reward crowdfunding platforms like Kickstarter and Indiegogo have also played an important part in helping to de-risk categories like hardware.

3. How do micro VCs differ from accelerators and angel networks?

Angel networks are active wherever there is a concentration of startup activity, such as the Bay Area, Boston, New York, etc. Angels invest their own capital and may invest as groups. In most cases, angels are not full-time investors. Angel.co is a good starting point to explore angel investors.

Most accelerators are built around three-month programs that were initially designed to help founders build products, but as the segment matures, many are more focused on helping firms to acquire customers. Startups are recruited in batches, usually twice per year, to make the vetting and pitching process efficient. The end goal is to help founders find seed-stage investors. A good overview of accelerators is available from SeedDB.

Micro VCs often co-invest with angels or follow accelerators, but micro VCs source, support and nurture deals via their own processes, too.

4. What challenges do micro VCs face?

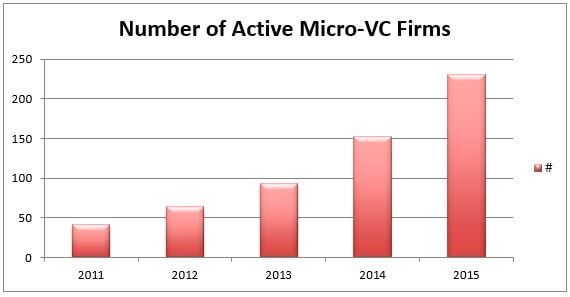

One major challenge is simply noise. Similar to the explosion of accelerator programs, there are now over 200 micro VC funds.

Figure: The number of active funds as determined from public filings on fundraising activity. Source: Past, Present, and Future of Micro VCs

Following investments into the later stages of a growing company becomes a challenge for many micro VC firms, which increasingly use SPVs (special purpose vehicles) to raise additional funds for specific opportunities, often at very discounted or no fees. LPs have noted that these opportunities can be an important part of investing in micro VCs, as they offer additional opportunities for returns.

Restricted by the operating budget generated by the relatively smaller fees that micro VC firms collect, some teams operate with one or two partners. This means that taking board seats at all companies is not practical, but it also means that firms need to be creative about finding ways to source and add value to their portfolio companies.

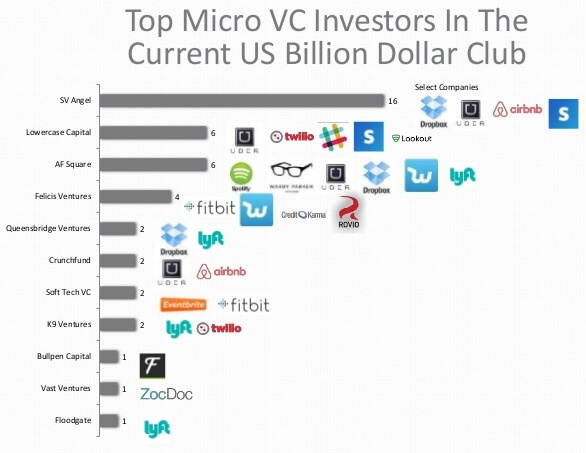

5. Who are the best performers?

As Samir Kaji highlights, many vintage 2013 micro VC funds have net internal rates of return (IRR) greater than 25 percent and MOICs (multiples on invested capital) of 1.5 to 2.5x. Another proxy for fund performance is the number of investments the fund has made in companies that are positioned to create an oversized return. There are some important assumptions, though.

Since MOIC is the current value of the investment divided by the price paid, it matters when micro VCs purchase their shares. A core assumption is that they invested during the seed round and this is increasingly easy to verify. Still, even in the figure below, not all investors have participated since the seed rounds, so they benefit from the unicorn halo but won’t benefit from their MOICs.

The unicorn proxy is also limited by two other important factors. First, since most companies are private, the assumption is that investors may have sold some stock, but not all, so their gains are mostly unrealized. Further, when one considers talk of dying unicorns and valuation corrections, one can see how this adds to the uncertainty about fund performance.

Source: Update on Micro-VC

Notes: First Round, despite the seed focus and success, is not listed because their most recent funds have been larger than $100m. Accelerators like YC are excluded. It’s not clear why Kapor Capital and Founder Collective are missing, as both are seed-stage Uber investors. However, the chart does give a sense of the connection between micro VC and some of the highest potential MOICs.

6. How do micro VCs differentiate themselves?

The vast majority of firms invest generally: that is, they look at opportunities independent of sector or theme. But specialist firms have begun to emerge as tech disruption expands across more sectors. This is somewhat consistent with Mary Meeker’s Internet trends report from 2015, where she looked at the relative impact of the Internet to date on various sectors.

The highest impact to date has been for consumers, though disruption continues. At the same time, government, regulation, policy thinking, healthcare, education, security, safety, and warfare are all estimated at half the level of impact. It’s interesting that, when you look at where micro VCs are specializing, you see a similar recognition. Fewer than 10 percent of current micro VCs have a stated specialization (there may be more that opt not to explicitly share focus areas). Some examples of sector and thematic specializations are:

- Urban.Us invests in startups that make city living better.

- Bolt seeks hardware-focused startups.

- Cowboy Ventures invests in consumer companies.

- Boldstart is only interestested in enterprise SaaS opportunities.

- Rock Health focuses only on healthcare investments.

- Learn Capital focuses on education opportunities.

- GovTech Fund focuses on firms that sell to local or federal governments.

Beyond the thematic focus, there is a good amount of innovation around process and platforms.

It’s also worth noting that traditional venture firms are not just ceding early-stage opportunities. Recently, Sequoia Capital revealed their “Scout Network,” which for years has quietly made early-stage investments via non-Sequoia entities in the hope that this will increase Sequoia’s odds of being able to lead later-stage rounds.

7. What’s the future of micro VC?

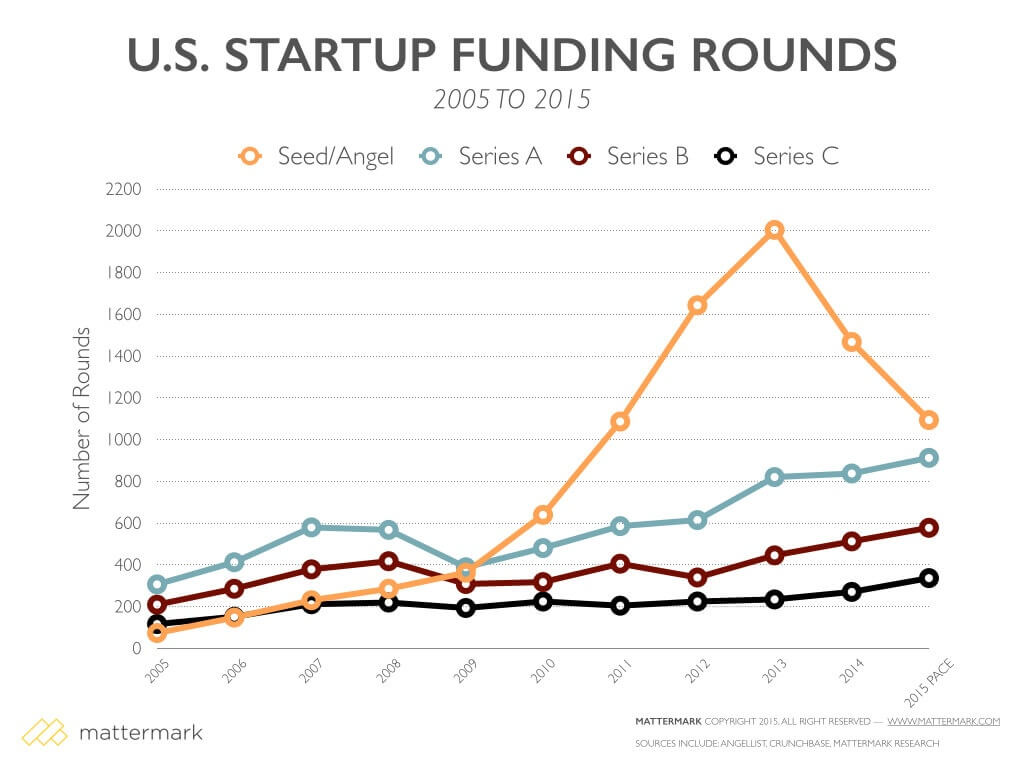

First, most micro VCs have deployed into an environment that saw a very sharp rise in the number of seed-stage deals. However, there has not been the same associated increase in growth-stage or later-stage deal activity, meaning that a larger number of seed-stage companies simply won’t get funded. This is likely to impact the performance of some micro VC funds.

Figure: The rise in seed-stage deals over the last few years has coincided with a surge in generalist micro VC funds, but there has not been an associated rise in series A activity, which is bad news for many portfolios.

Source: Mattermark.

As benchmarks emerge, the next question is: who will continue to fund micro VCs? So far, traditional VC LPs have largely been institutional investors and even funds of funds (which are in turn aggregating investments for their institutional investors). But micro VCs are also supported by family offices and high net worth individuals. So one major question is: what is the capacity of family offices and high net worth individuals to continue to support the growth of micro VCs into subsequent funds as is common for institutional LPs?

Corporate ventures might also become more active. To date, they’ve set up their own funds and partnered on accelerators. It’s not a big stretch to see their participation in more specialized micro VC funds. The same is true of larger venture funds that have displayed interest in “feeder” relationships where LP roles enable them to secure access to de-risked deals for early- or late-stage investment.

Beyond the LP questions for funds are other emerging sources of competition for allocations, that is, how much money funds can invest in the deals they’d like to do. A number of successful firms have co-invested with accelerators like YC, but YC now has a $700m later-stage fund. While it’s not intended to lead seed or A rounds, it is still likely to create some shifts in how money is allocated to their alumni companies. Similarly, angel.co announced a $400m seed fund to support investors on their platform. This too will potentially create less room for micro VC funds.

Most recently, a new early-stage coalition was announced to focus on energy. Led by Bill Gates, The Breakthrough Energy Coalition includes a number of well-known angels, VC funds and early-stage investors such as Marc Benioff, Jeff Bezos and Richard Branson. We suspect that this type of activity might cause more mission-driven organizations, like foundations, to look more closely at how to invest directly or via funds into the seed-stage space.

Finally, there is the question of fund economics. Some of this is driven by the math of allocation models where certain amounts of capital need to be “put to work.” Perhaps this means doing more secondary market deals to get access. Or maybe something completely different from the SAFEs, CNs and seed equity rounds that put founders onto the path of raising more capital. Indie.vc is rethinking the model, as illustrated by their first term sheet, the SACS or Simple Agreement for Cashflow Sharing.

Similarly, public benefit corporations may further impact how founders think about their relationships with investors as they formally add obligations to other stakeholders. Kickstarter was one of the most visible later-stage conversions, but we expect that more firms will want to build their mission into their legal structure, just as some will prefer SACS over SAFEs.

Just as winter is always coming from seed-stage companies, so it is with new and emerging micro VCs.

Join thousands of business professionals reading the Mattermark Daily newsletter. A daily digest of timely, must-read posts by investors and operators.

This guest post is by Shaun Abrahamson of Urban.us. He’s on Twitter or LinkedIn.