Editor’s Morning Note: After a rough 2015 and no better start to 2016, investors are finally warming back up to Box.

Shockingly, finding interesting pictures of boxes leads to a very shallow pool.

Happy Tuesday, friends. Today, Google is unveiling its best iPhone fanfiction, and Dreamforce is threatening to make San Francisco even more unlivable, so you and I can afford a minute to stare into the eyes of an unforgiving market.

That, and I am working on our third quarter venture capital report, which means that we are under a time squeeze.

This morning, we’re looking at a massive rally in the value of Box, a public SaaS company, and what it might mean for the value of the startup ecosystem.

Up From Down

Box matters, as it is an effective barometer for public-market sentiment regarding SaaS companies, and the recently public. As you can imagine, given the number of SaaS startups that eventually need to go public, how they are viewed by regular investors matters.

So as Box goes, so too does the IPO market for yet-cash-burning SaaS companies ramping towards profitability while maintaining growth rates in-line with expectations. (That’s a lot of companies, after all.)

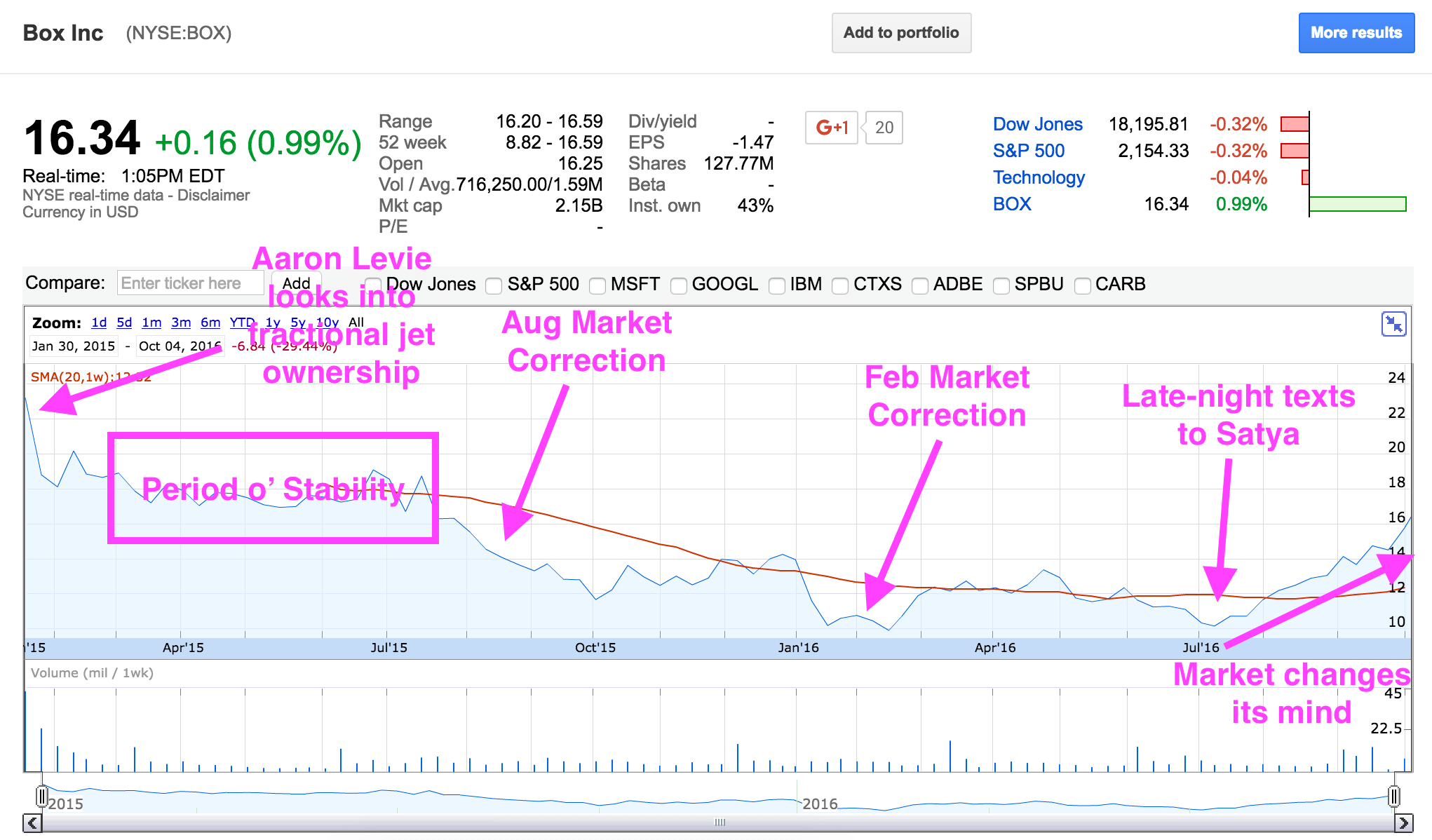

Building off of this prior thought, here’s a quick historical rewind of Box’s life as a public company:

It’s that last bit that we find the most entertaining. Over the past few weeks, the following has happened:

- Box got back over its IPO price ($14) for the first time since the start of the year.

- Box erased nearly all losses that ensued since the market’s August 2015 correction. That correction, you will recall, was the first shockwave that dented private-market sentiment. Box’s revenue repricing at the time likely did not help your local startup price land new capital where they wished.

- Box’s share price is now doing what its revenue has been; this reverses the former trend in which Box’s revenue would rise, and its value would fall.

Notably, I don’t think you can now call Box’s IPO a failure and field a solid argument to support the view.

Box’s rally has happened quietly. As you can see in the chart’s most recent weeks, the company’s gains have come on the back of a consistent trend, and not massive, single-day spikes. That means fewer headlines and attention. (If you really want to command a media cycle, collapse or explode your value by 99 percent in a day; CNBC will call.)

How Far Up?

How far has Box risen? The company traded at least as low as $10.15 per share this summer. Today, at $16.35, it’s up more than 61 percent in just a few months.

That means that the value of recurring revenue at perhaps the most important market analog for private SaaS companies has made a massive comeback. That may help smaller firms demand, and even command, higher valuations from private investors.

Inside baseball yes, but important inside baseball all the same.

Moving forward, if you want to track the value of recurring revenue on your own, you can do so quickly using the following rules of thumb:

- Box shares down, Box revenues up: Double squeeze on the value of ARR; recurring revenue’s value falls.

- Box shares flat, Box revenues up: Single squeeze on the value of ARR; recurring revenue’s value falls.

- Box shares up, Box revenues up: Potentially no squeeze on the value of ARR; recurring revenue’s value may rise.

The final category depends on rates, of course: If Box’s recurring top line spiked by 100 percent while its shares grew a more modest 1% in value, you can do the ratios yourself.

We can now put Box aside until it reports earnings, at which point, we’ll do another workout of what the value of ARR in fact is.