Editor’s Morning Note: Some recent tech IPOs are looking to bring in more cash. Here’s what the market thinks.

Area Unicorn CEO Discusses IPO Pricing Strategies.

Twilio and Acaia Communications’ IPOs have been successes for the technology industry. Both companies have rapidly grown to a multiple of their debut price, and both have pushed oxygen into the year’s IPO crop.

Following a determinedly lackluster year for IPOs in 2015, the technology industry had hopes for a better result in 2016. In terms of volume, it appears likely that 2016 will fail to meet 2015’s low bar in terms of volume.

Which puts all the more pressure on the standouts. And Twilio and Acacia have been nothing if not standouts.

However, both want to raise capital at a higher per-share price and ride out their lockup periods with low volatility. That’s why both have proposed, and one has executed, an offering of this sort—selling both primary shares from the company itself and equity from other shareholders at once—at a higher price

Let’s examine the lesson.

Two Goals, One Action

Twilio and Acacia Communications both proposed to sell more of their companies, but their new offerings did not depend on the companies themselves putting up most of the shares. Instead, other shareholders can sell their equity in the deals.

This accomplishes two goals:

- It generates more cash for the company through the sale of shares.

- It provides controlled liquidity to other investors, potentially lessening later price chop as long-term shareholders look to diversify their holdings after the lockup period expires.

A great set of results, if you can get them. And you can get them with a strong market price. To wit, here are the raw numbers from both companies:

Acacia Communications

Round one:

- IPO Price: $23

- Shares sold (Discounting underwriter option): 4.5 million

- Capital raised: $103.5 million

Round two:

- Per-share price: $100

- Shares sold (Discounting underwriter option): 4.5 million

- Capital raised for company and shareholders: $450 million

- Percent of capital raised, raised by company: 27 percent.

Twilio

Round one:

- Initial IPO Price: $15

- Shares sold (Discounting underwriter option): 10 million

- Capital raised: $150 million

Round two:

- Per-share price: Not set!

- Shares sold (Discounting underwriter option): (Filing says a max of $400 million)

- Capital raised for company and shareholders: (Filing says a max of $400 million)

- Percent of capital raised, raised by company: 12.5 percent ($50 million)

As you can see in the first case, Acacia raised a huge amount of new capital for itself and its shareholders at a far higher per-share price than it debuted at, allowing the company to leverage its success to date.

Twilio will sell its next traunch of shares at a much stronger price than it first went public. (The company has traded as far as the high 60s since its offerings.)

All good? Well.

Results: Capital And Some Whining

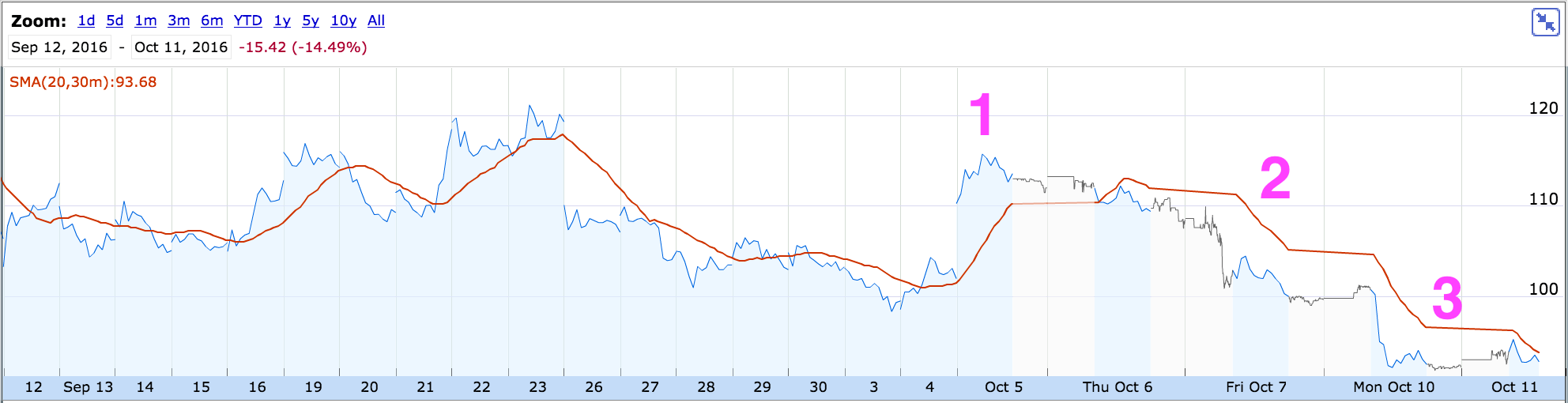

We can use a chart to make the point.

What follows is the Google Finance chart of Acacia’s share price over the past month or so. The relevant occurrences are labeled. See if you can guess what happened around the timing of each:

If you went with the first being the announcement of the offering, the second being later reaction to pricing, and the third recent trading, congratulations! You win nothing but these great 20-20 Hindsight sunglasses!1

What the chart shows is that the market isn’t, by definition, opposed to such moves, but when the company announces a per-share price that is around $10 less than the prevailing expectation, it can get rough.

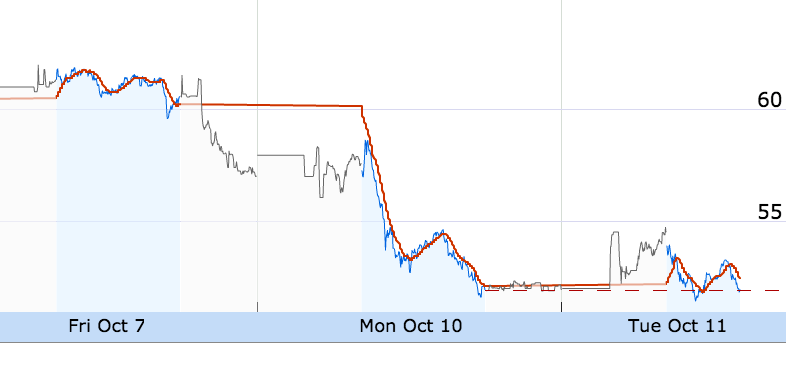

So what happened to Twilio after it announced its offering? Here’s a taste:

To summarize the egg and floor: Splat.

—

All this is intra-baseball, but it helps us understand the true cost of pricing an IPO low to start, in hopes of garnering a strong first-day performance. It’s smaller than you might think, provided that you can execute a second offering at a far higher per-share price. You are in effect, then, capturing, in part, the positive dollar value that could have been wrung out at IPO perhaps, later, when it was safer to collect the dollars after a period of share-price appreciation.

So did that company really leave that much money on the table? Maybe. But not as much as you might have thought.

- You actually don’t. Tough.

Disclosure: Mattermark’s CEO Danielle Morrill was an early employee of Twilio. As whenever Mattermark’s editorial group writes about a topic that may present a conflict of interest, the company itself, and its constituent investors have no say in our work.