Data-Driven Deal Making

Discover, prospect, and track the world’s fastest-growing companies and investors.

No commitment, no credit card required.

Company Profiles

80+ fields per company including geography, industry, revenue, personnel, funding, and employee growth.

Key Personnel

Identify the right contact based on title, function, and seniority.

Growth Signals

Get smarter about outreach by monitoring changes in team size, web traffic, media mentions and more.

Using Data You Can Trust

Where We Get Our Data

We leverage machine learning, web crawlers, primary sources, and natural language processing to extract data from millions of news articles and websites daily.

Our team of in-house analysts verify the data every day - so you can close deals with conviction.

Discover new opportunities

The world’s business information in one place, filterable and sortable. Mattermark makes it faster and easier to source the best deals.

Track Success

Search company and investor profiles for deep insights into their growth and performance over time. Break the cycle of doing business without good data.

Stay Informed

There are 300+ million private companies in the world. Saved Searches, Custom Lists, and News Notifications make it possible to keep tabs on the ones that matter most to you.

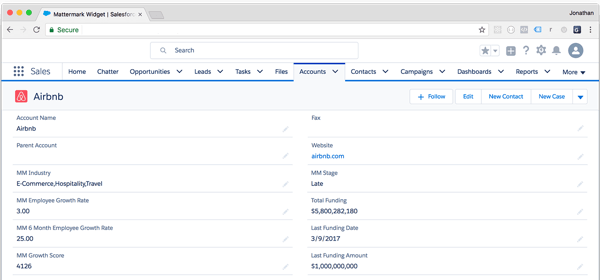

Automatically Enrich Leads in Salesforce

Get actionable insights by syncing over 80 informative fields to help warm leads and power conversations from first touch to deal close. Get all the relevant information from inside Salesforce, and apply triggers and actions to any lead, opportunity, or other object. Learn More

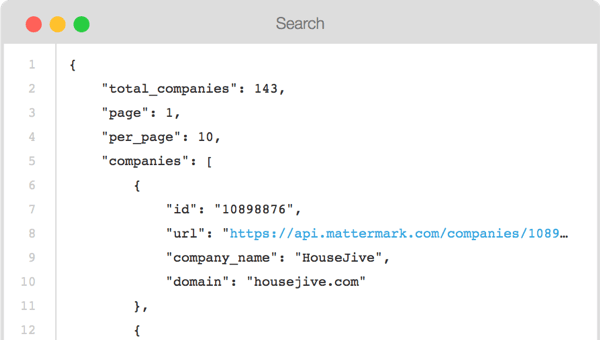

Customize your Experience with API

Our API provides data on millions of companies. In just minutes, you can integrate Mattermark with your products, systems, and business processes. Create your own models and scoring algorithms to fit your business. Learn More

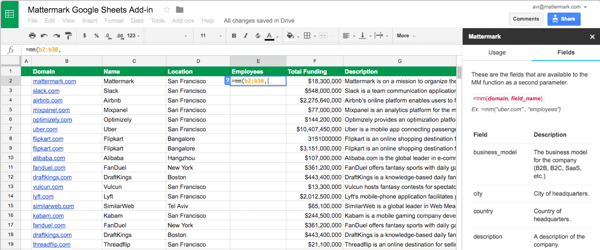

Export Mattermark Data to Spreadsheets

Pull Mattermark data directly into Google Sheets or Microsoft Excel to add live updated company Growth Scores, location, funding, employee count, and more into your spreadsheets. Learn More

Deal Professionals Use Our Data

Investors

Surface new companies and better deals, faster.

Sales / BD

Dramatically reduce prospecting time and identify future customers with Mattermark.

Professional Services

Research markets, understand competitive landscapes, and deliver to clients quicker.

4 Million Companies

20 Million Key Contacts

Start contacting your target list today

No commitment, no credit card required.

Right data. Right format. Right now.

- Developer Tools (REST and GraphQL APIs)

- Web-based Data Browser (CSV and PDF)

- Spreadsheet Plugins (Excel and Sheets)

- Browser Extension (Google Chrome)

- Mobile (iPhone lookup app)

- CRM Integration (Salesforce)