tl;dr: Just because you can discount a cost doesn’t mean it’s gone forever.

Before we dive into a long look at the first quarter of the year and all its financial glory, I want to take a minute to talk about money.

We are heading into an incredibly interesting period in the technology business cycle. There are lots of unicorns, and no IPOs. Ergo, there will be IPOs this year. You’ve read a dozen articles about the current financial shape of our late-stage startups. If they go public, you’ll get the full download. The figures that are finally reported may differ from what you thought you knew, or what you were told.

Let’s talk about what is real, and what matters.

Small Companies With Big Ambitions

Looking at smaller, younger companies, investors, analysts, and journalists often measure their performance on a cash basis. This is an intelligent way to go about vetting a startup. What you care about is how quickly more money is coming in, and what that new revenue costs in terms of cash burn.

In this sense, many things are often not taken into account, like share-based compensation. Issuing shares to an employee as part of their larger compensation package is normal, and a smart idea. But it often doesn’t require a short-term cash expense. So, in the case of startups, non-cash costs are often ignored.

However, modern accounting rules (GAAP) are stricter. What’s fun is the ruleset applies more to older companies with public shareholders. So, startups get to say bizarre, and fun things like “we’re margin-contribution positive,” and “we have positive unit economics in 40 percent of our locations, discounting for corporate expenses.”

You might giggle, but this stuff confuses non-financial kids.

But the bullshit here matters, because it’s not all bad. Yes, quickly growing companies will often lose money as they scale; so long as the curves eventually cross, all is well. It’s when the bent metrics are regaled as straight GAAP that I get irked. In the meantime, akin to children, we allow startups more latitude to explain their performance.

No harm, no foul.

Public Companies Mind The GAAP

Once a company is public, however, things change. This is when non-cash costs are not only strictly tracked, but repaid.

If that doesn’t make sense, keep in mind two things: GAAP is strict, and you can’t avoid its dictates—regardless of whether you want to or not. You are now playing by big kids’ rules. And now all that share-based compensation, to continue the example, was merely unpaid dilution for your existing shareholders that you have to pay for.

What does that mean? It means you pay for past distributed equity-in-lieu-of-cash in two ways: Share buybacks and dividends.

If every share you created and released has a dividend attached to it, you have effectively increased the coupon cost of your own equity. Congratulations! And, as companies like Microsoft have shown, buying back your equity can be a lovely way to constrain your earnings to a smaller share pool, thus boosting your earnings per share.

You have to buy back, with cash, the thing that you gave away to avoid using cash. And, now, it’s probably worth more.

This manifests in mature companies paying for their prior growth with current and future cashflows. This is not a sin. But it is something to always keep in mind when looking at a company you might want to work for, or the company you run. You can delay some costs, but you never ignore them forever, unless your firm dies.

The only functional counter example are firms that grow sufficiently quickly over huge periods of time that investors do not demand a dividend from them, even as they mature into titans. That’s Google, and Amazon, for example. But nothing lasts forever.

Cash For Shareholder Return

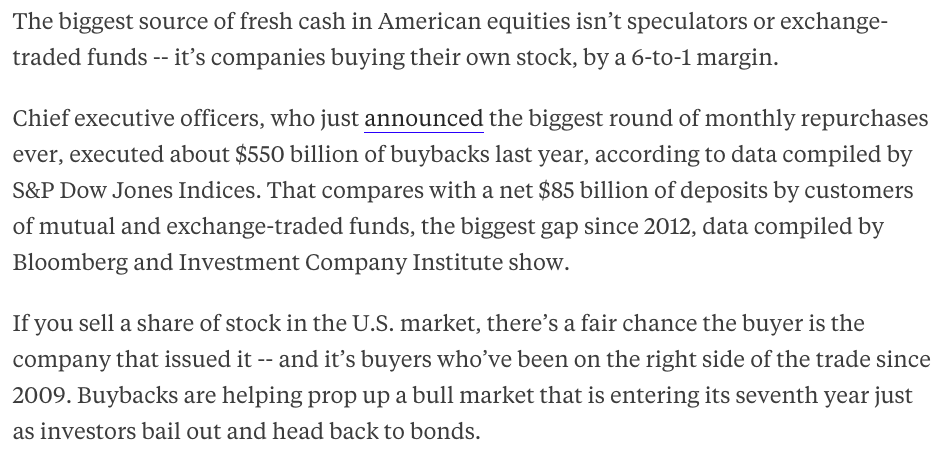

A friend of mine shared something with me recently that took me by surprise:

This underscores our point. You want to talk about why non-cash costs are often deferred cash costs? There it is in spades.

None of this is to say that companies should not repurchase their own equity. It’s a perfectly intelligent way to reward long-term investors by providing more earnings per share for their held shares. That’s great. But it also does remind us why Twitter, using GAAP metrics, lost more than a half billion in its fiscal 2015, but reported adjusted net income of $276.6 million during the same period.

Why bring all this up? We may be in an IPO desert, but eventually this year some unicorns and other private tech companies will go public. The market will have to square their past notes on their financial performance with their GAAP figures. I’m not exactly expecting another Groupon, but I do expect some pain and testy interviews.

For us peasants, it’s enough to understand what true profitability is. Stay alert: The era of bullshit is fading.