Editor’s Morning Note: Oh ****, Fed hikes are about to happen.

“Great companies can always raise.” “I’ve not changed my investment thesis.” “Things aren’t that bad.” “Buy the dip.”

Happy “End of Cheap Money Day,” friends. Today, the Fed is expected to raise its short-term benchmark interest rate from 0.5 percent to 0.75 percent.

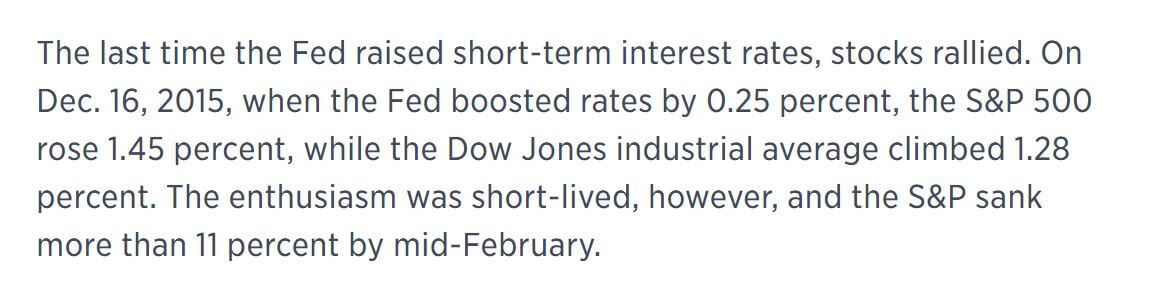

When the Fed did something similar in 2015, as CNBC notes, things got a bit rough:

If the past is a preamble, we may be in for an interesting few months.

Why talk about government policy here on Mattermark? Because there is only one global economy, and what the Fed does today may change the direction of the flow of money and its velocity.

There’s a lot in startup tech at the moment that is predicated on there being more money available: Startups have set their hiring, growth, and burn budgets on the assumption that good performance will yield access to more capital.

You can conjure how it may be problematic if that reality changes.

Rewind The Tape

Back in 2014—one of the stronger years for unicorn creation—a meme went around Silicon Valley that all was about to get worse.

I wrote a trio of articles in 2014 on the exact topic. The headlines are decent summary: “Winter Is (Probably) Coming (Soon),” “The Long Fall,” and “Burn!”

The brace worked on the question, to some extent, of what happens when the price of money changes. Here is what you should expect, at least from what I can glean from a few dozen conversations over the past few years:

- When the Fed raises rates, it will make certain asset classes more attractive.

- That will limit the amount of global capital that is “bored.”

- This changes the hunt for yield, likely diverting some capital away from riskier assets.

- Speculative investments (like venture capital) will become less appetizing to monied pools.

That could mean venture capitalists, currently standing up from an LP-led bender of a year, could be in for a tougher spot. If that’s the case, there could be fewer dollars available for startups in the future. That means a more intense battle among startups for the same dollar. That, in turn, shifts power back towards the venture community—a phenomenon already underway—forcing lower valuations, more onerous terms, and other things that venture kids claim to dislike, but actually love, as it means they make more money.

(The profit motive, contrary to unicorn P&L statements, isn’t a sin.)

Regardless, all the above is well-known in the market. None of this is a surprise. However, while other asset groups and industries may have priced in the coming change, I am not convinced that the broader venture and startup landscapes have.

The featured image wasn’t just a goof, in other words.

—

If the Fed doesn’t raise rates, it’ll be odd. This one has been expected. And markets are at record highs while the economy improves. There has even been some movement in oil prices.

Now, if the markets lose their collective mind after the raise, we have something new to chew on. Otherwise, let’s masticate this old news and get to what’s next.